A GSE, Portfolio & Position Commentary

Reviewing an eventful quarter

Investing is humbling. Quite often the enforced humility is accompanied by an acute pain in your pocketbook.

While I have joked, on and off, about starting a fund with various whimsical mandates, I think the most compelling idea would be to invest on the basis of the stocks that I have discussed, but not invested in. A short summary of these below:

I won’t take any credit (even if it’s in a negative sense) for Fannie Mae and Freddie Mac. Both securities currently trade OTC, with the US government effectively sweeping 100% of their profits into Treasury’s coffers. I have seen a decent case made for the current price being offered by bookmakers on a Trump Presidency being a value; little did we know that the ultimate bet on that outcome was the GSEs!

I continue to follow both Fannie and Freddie’s story with the hopes that they eventually get rebirthed from the government’s present conservatorship. It’s not even that I want to participate in the equity (or prefs for that matter) pre-reorganisation. Government asset sales, reorganisations, and demutualisations have been a rich field for investors since time immemorial. This becomes doubly true when the underlying businesses are advantaged and durable. The origin story of how Freddie became publicly traded is instructive.

Prior to 1988, ownership in FMCC, by law, could only be held by a Savings and Loans Bank (S&L). This wrinkle reflects the pre-privatision history of many naturally occurring monopolies in financials - unsurprisingly, the self-interested institutions that were the GSEs major counterparties also owned them. In 1988, with many S&Ls desperate for capital and bi-partisan support across the aisle in Congress, arrangements were made for ownership to be made available to the public.

It would be incorrect to call this particular instrument “stock”. Technically FMCC was a ‘participating preferred’, entitling owners to the first $10M of distributable owner earnings every year, and 90% of the amount thereafter. Prior to 1988 FMCC also traded purely OTC, basically by appointment. The opaque and illiquid nature of these securities massively affected their valuation. Before being listed on the NYSE it traded for 8x trailing earnings.

This unusually low valuation (even for the late 1980s) was set against the following context:

From 1970 through 1987, the market for conventional residential mortgages grew at a compound annual rate of more than 13% and never at less than 5.5% a year. Not bad, but what makes the business outstanding is the paucity of competition. Fannie Mae is the only other major player; the chief difference between them is that Freddie resells virtually all its mortgages, while Fannie holds onto a substantial amount of them. Together, Freddie and Fannie control 90% of the market. Says Buffett: ''It's the next best thing to a monopoly.'' The future of the Freddie-Fannie family duopoly looks encouraging. The market could expand for years to come. So far only 33% of conventional residential mortgages are securitized, leaving plenty of room for growth. Moreover, savings institutions will soon have another powerful incentive to buy more mortgage-backed securities. In 1990 savings banks and S&Ls holding ordinary mortgages will be required to maintain bigger reserves against loan losses than if they owned a diversified portfolio of securitized mortgages. Of the two, Freddie may be the better bet. Over the past decade, its return on equity has averaged more than twice Fannie's. Because Freddie's managers buy only top-quality mortgages, Freddie's delinquency rate for conventional fixed-rate single-family mortgages is a mere 0.4% of its $230 billion portfolio. With holdings of similar size, Fannie has 1.1% delinquencies. President Leland Brendsel and the other Freddie Mac managers minimize their exposure to interest rate spikes, which hurt mortgage bankers by raising their cost of money while lowering the price of mortgages in the secondary market. Brendsel keeps only $15 billion worth of mortgages on the balance sheet, vs. Fannie Mae's $102 billion.

A WARM TIP FROM WARREN BUFFETT: IT'S TIME TO BUY FREDDIE MACS, Fortune Magazine 1988

To summarise:

The underlying market was growing at 13% on average for the past 17 years,

Unusually high returns on equity were made possible by an asset light operating model,

The market for insuring residential mortgages was a natural duopoly. Both Fannie and Freddie enjoy a funding advantage via low cost financing from Treasury,

Known industry changes would support additional demand for mortgage-backed securities (MBS) into the foreseeable future.

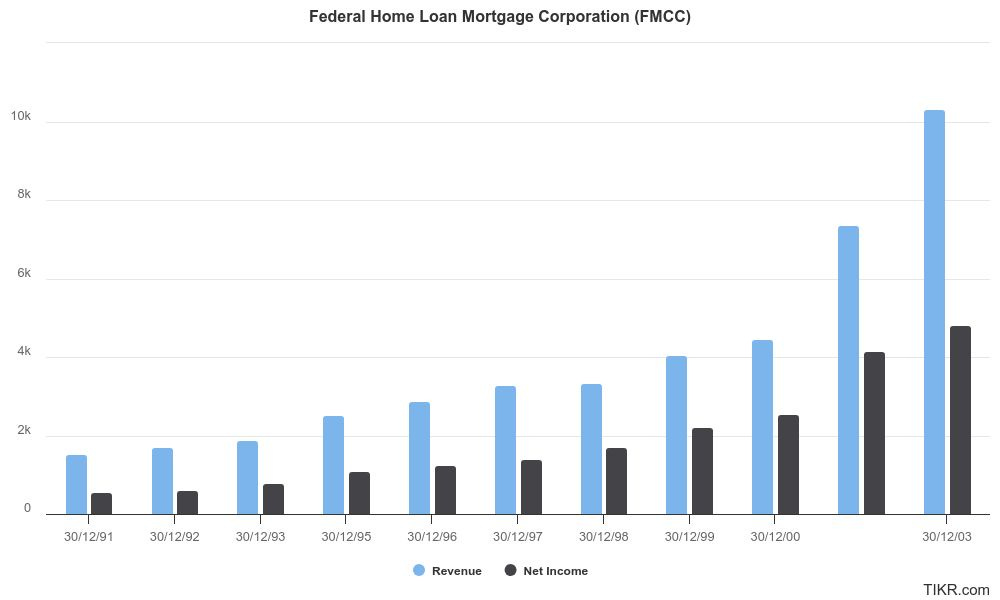

I have been able to find a bit of secondary data on Freddie’s financial performance post-listing on the NYSE, but take this with a grain (maybe a spoonful) of salt:

Buffett described the opportunity at the time:

''Freddie Mac is a triple dip,'' says Buffett. ''You've got a low price/earnings ratio on a company with a terrific record. You've got growing earnings. And you have a stock that is bound to become much better known to equity investors.''

Munger had a somewhat less nuanced, but equally enthusiastic, stance:

''I can't think of a more tangible compliment to the stock than to buy every damn share we are allowed to.''

You won’t find it a particular surprise that at least a few of my more recent investments rhyme with this setup - see below:

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.