Automatic Bank Services Limited (SHVA) - Held

Another compelling idea in Israel

A quick note before we get stuck into the details: this is a pretty illiquid situation. Somewhere between $50,000-$200,000 USD worth of stock trades a day. Naturally, this has implications for short term price movements. As always, do your own work before making any investment decisions.

I have been doing a bit more work on - and putting some capital to work in - Automatic Bank Services Limited (SHVA). It fits nicely into my general framework. The opportunity is seemingly compelling, and the the thesis is straightforward.

| LinkedIn")

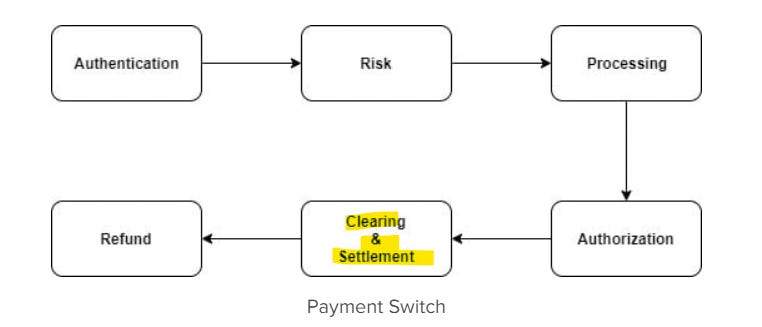

SHVA operates the national payment switch in Israel. Simply speaking, this is a service that facilitates communication between customers, merchants, issuers, and acquirers. They also operate the ATM system domestically, allowing cardholders to withdraw cash from ATMs not operated by the financial institution that they bank with.

This business has traditionally been monetised in two ways. Firstly, SHVA charges a $ value per transaction. Secondly, they charge merchants a annual fee for the use of various payment terminals. To a much lesser extent they derive revenue from other value-added and data services (not dissimilar from Visa and Mastercard).

Importantly, the core payments infrastructure SHVA operates is a natural monopoly. Conceptually it is a local network - the connection of so many different parties to a transaction means that establishing a competing service is extremely difficult, verging on impossible. Aggregating the merchant side of the network is especially tough for any emerging provider. As is often the case with such advantaged positions, the addition of every additional party to a transaction done through SHVA’s network makes the value of that network greater. Once established, a payment network not only brings efficiencies to those taking advantage of their services, it also makes the establishment of another regional switch expensive.

In some Western jurisdictions settlements (outside of credit cards) are often operated by some sort of mutualised body that is owned by that country’s leading financial interests (for instance, all kinds of payments in Australia are settled by AusPayNet, a limited liability company partially owned by the large banks, credit unions, and building societies). This was the case for the longest time with SHVA.

A little history

SHVA was established by Israel’s leading banks in 1978. As part of a series of reforms aimed at increasing innovation and competition, in 2019 the largest four banks were all forced to reduce their stake in SHVA to 10% each. Remember this for later, it will be important. For those of you who follow the newsletter closely, this was part of the same set of legislative efforts that saw Tel Aviv Stock Exchange become a publicly listed company.

The other important historical footnote worth mentioning is SHVA’s relationship with Visa and Mastercard. In the past, Israel’s financial regulator (at that point the central bank) encouraged Visa and Mastercard’s entrance in the Israeli market. The prevailing wisdom was that a competing payment switch would lower prices for merchants. More on pricing later too. In any event, both were convinced that the opportunity was likely not worth the effort. Neither has ever made any significant head way in establishing a competing payment switch - but both operate the prevailing payment rails. After all, most Israeli citizens will travel overseas at some point.

Consequently, Visa and Mastercard are both significant shareholders - owning a 10% stake each. The reason for my prominent note on liquidity should be pretty clear by now. While the market capitalisation of SHVA is a touch higher than $160M USD, more than 60% of that stock is locked up by shareholders who have zero interest in monetising their ownership - or in V and MA’s case, maybe don’t even know they own it.

The consequence of SHVA’s idiosyncratic history (geez, everything I write about is like this) is that it hasn’t truly been run for profit until very, very recently. This odd history manifests into SHVA’s current operations in two very important ways. Firstly, their products are priced at rates far below Western comps. Before 2023, the last time SHVA increased the fee they charge for the collection and authorisation of payments was in 2014! Before the 2023 changes, these rates were 1/5th of what V and MA would charge for the same service. Untapped pricing power anyone?

These charges, generally, exhibit another peculiarity - they are charged on a $ per transaction without charging a % of the transaction value. This is a decided disappointment in SHVA’s business model. It means that the company only benefits from a greater velocity of card payments. This has definitely not been as issue for them so far - almost 80% of men and women above the age of 15 own a credit card in Israel. However, it does leave them somewhat susceptible to inflationary pressures. The current geopolitical situation has engendered higher domestic inflation than what the rest of West is currently experiencing. Their only remedy to this is the blunt use of price taking. This incurs the ire of the regulator.

Secondly, there are a slew of additional services that comps have developed over the years that SHVA hasn’t pursued. This is changing and two important catalysts have come to bear already. Firstly, the appointment of a new management team took effect in mid-2021. This saw the installation of Eitan Lev-Tov as CEO. Lev-Tov has an impressive resume with extensive experience in technology broadly. Since his appointment, he has been dynamic. Secondly, and just as importantly, management has been given equity in the company. While this has materialised as a higher near term expense, I believe it will better align management’s interests with those of the shareholders - especially the minority shareholders.

For a more in depth look at the unit economics and the business developments that happened pre-2022, you can check out the following post on VIC - and Jeremy Raper’s Seeking Alpha write up. In the interests of not rehashing already covered ground I’m going to focus on the opportunity going forward…

The current opportunity…

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.