Buyback Annual Letter 2024

Another year in markets

With a few trading days left in the year, it is my usual practice to reflect on the year that has been.

Looking back on the last couple of annual of letters, I feel honour bound to stick to my usual opening which is to both eschew macro forecasting but to then comment on it nevertheless.

Macro

The purpose of economic forecasting is to make fortune-tellers look good.

The economic outlook is always hazy. As to whether inflation is higher or lower in the next year I couldn’t possibly say. The same applies to any of my would-be predictions on what direction the stock market goes over the next day, week, month, or even year. This certainly doesn’t stop me from expressing certain bias’s in my personal portfolio around interest rates, and currencies.

As most readers will know I currently live, am a native of, and earn a living in Australia. Most (although not all) of my earning power is denominated in Australian Dollars - a rapidly depreciating currency I fondly refer to as the Pacific Peso. My practice since at least 2016 has been to - not unlike an Argentinian on payday - exchange my Australian dollars for foreign assets at the earliest possible convenience. This requires some explanation.

The Commonwealth (the Australian Federal Government), has been stuck in a policy straightjacket for many years that has resulted in, and will continue to affect, a structurally weaker domestic currency for. The policy decisions coming out of the Covid re-openings has only exacerbated the consequences of this folly. Of course, the double sin we experience down under is the religion of residential property ownership, and the innate desire for every Australian to live at the expense of his or her neighbour. The latter attitude also seems to be seamlessly adopted by those who immigrate here. Long gone are the days of the defiantly independent larakin. Enter the age of the life-long welfare recipient and/or civil servant.

The stated intent(!) of the Commonwealth is to ‘sustainably grow property prices’. Don’t mind that we already experience some of the most expensive property prices on the planet - we’re only pipped by places like Hong Kong and New York when you compare residential property prices to local incomes. On this point I will not argue with the globalists. Citizens of a country (especially those in the top 1% of incomes!) should be able to afford decent housing in the country that they are born and pay taxes. Defending local asset prices (especially residential property) has been at the core of so much of our economic mismanagement.

To keep the property circus running we’ve done things like import many more people than we can possibly house, and given government guarantees to 2% down payments (promoted by our Prime Minister no less), which has led to most of the productive elements of the economy being backed by it. Without needing to derail this more than it already has been, when given the choice between defending the currency (through reasonable interest rate policy for example) and defending local asset markets, our authorities will inevitably pick the latter.

The decline in the Australian Dollar against the United States Dollar has been the third largest contributor to my portfolio this year. While many Americans are concerned with inflation in their own markets - a fear well founded on the inflationary impulses of the incoming MAGA Republicans - Churchill once said that:

‘[D]emocracy is the worst form of Government except for all those other forms that have been tried from time to time’.

I fear that the same is true of currencies.

Equity Markets Generally

The general consensus is that there is very scant value to be found in the US equity markets. I would certainly agree with that sentiment and my opinion on what to do about this has not changed. If we’re presented with a dearth of earnings power plays in the world’s largest and deepest equity market than the remedy to this state of affairs is to either find categorically different types of investments, or fish in different markets altogether. Excepting for the moment that I have done a bit of both, I have still been able to make perfectly acceptable investments in two new US business in the back end of the calendar year. If you find yourself devastated over the apparent lack of opportunities you may just have to look a little harder.

In any event, an intelligent investment program is essentially opportunistic. Market participants don’t get to make demands of the market. To the contrary, markets avail opportunities to the prepared mind. An overly rigid orientation obstructs occasional ‘pretty aggressive conduct’. The latter is of course a necessary (although not sufficient) condition for effectively seizing opportunities. In my experience opportunities do not come along at convenient interludes. If success to the upside is usually catalysed by a myriad of factors working to a common outcome, than the same is often true on the downside as well. Herein lies an intellectual tension - opportunities come about because of a collection of circumstances which are unfamiliar.

Risk

The most insightful thought I have come across this year have come via a series of tweets by user @turtlebay_io:

Buffett is fundamentally an oddsmaker and risk manager. He’s only written about it a few times, and what he’s written has generally been ignored (despite being some of the most useful stuff I’ve read). But his interest/aptitude is clear: portfolio construction, obsession with non-transitive dice, love of bridge, nightly talks with Ajit, weird interest in outlier events, thoughts on sizing and correlation, his lack of losses (despite running a balance sheet full of unknown liabilities), his willingness to take on quirky but financially insignificant side bets. Even that one bet he made in Vegas when passing through the casino lobby.

Putting aside the enigma that is Buffett’s approach, the general premise here prompts a little introspection. Certainly, the further I go along the more I appreciate the primacy of risk as opposed to return considerations. The two concepts do not, however, enjoy a correlation or even direct relationship in every particular instance. To be sure, the cheaper something is the less downside risk it has. At the same time, however, it also has more return potential if you assume that values mean revert over time. Returns in individual securities are subject to starkly non-linear outcomes, especially on the upside. Certainly the positive ones that are reasonably identifiable ex-ante are an even scarcer commodity. To then find the few situations that also present significant downside protection - we’re talking about finding a needle in a field of haystacks.

This kind of orientation might lead one to a concentrated approach. While I don’t quarrel with this, I think the deeper point is to (and I’m repeating myself here) be opportunistic. Perhaps we find ourselves in an environment where there are an enormous opportunities in a plentiful number of securities. Perhaps we find ourselves in a very cheap general market. Perhaps we find ourselves in a rich market with idiosyncratic opportunities. It’s certainly no guarantee of success to say that one should remain open-minded, but you can almost certainly guarantee mediocrity by being mentally inelastic.

Irrespective of what labels we adopt, or the ones that others heap upon us (quality investor, compounder bro, business analyst), we are inescapably risk managers and odds makers:

The first rule of investment is don’t lose money. The second rule is don’t forget the first rule, and that’s all the rules there are.

Over a long period of time, our success is inextricably linked to not having catastrophic losses. Buffett is perhaps the business person most aware of this fact in living memory. To be sure, he has has temporarily disappointing periods. It’s also true that he has underperformed several of the large indexes for long stretches. Even the managers with which he has outsourced a piece of the capital allocation function have had mixed success (one is almost certainly some shade of charlatan).

His asset mix during the partnership days is instructive. There were long periods where BPL’s portfolio turnover was extremely high, and the number of securities owned was large. There were also short periods of time when the portfolio was extremely concentrated in unusually attractive issues. When markets moved higher, and values were scarce, the selection of portfolio positions skewed toward market neutral situations. At points he implemented the use leverage. The partnership’s ability to move portions of its funds to ‘control’ situations enabled him to be able to set his own marks (in a conservative fashion no doubt) - a nifty trick implemented to great effect by private equity in recent decades.

When Buffett took over Berkshire Hathaway, and subsequently rolled in a number of insurance operations, he gained exposure to positive carry leverage - although in subsequent years the cost of float may have been closer to 2%. As Munger once quipped:

You don’t need to be a genius to know that if you buy businesses earning 12% and borrow at 2%, you’re going to have a good outcome.

In subsequent decades he was able to negotiate sweetheart deals out of distressed situations (GEICO, Fruit of the Loom), and pursued a form of soft, collaborative activism (The Washington Post, Cap Cities), amongst many other idiosyncratic approaches to capital allocation. The ‘true north’ always remained the same - a fastidious and ruthless approach to managing risk and finding value.

The Truth is Never Simple, and yet it is

The truth is that there are gradations of managed risk, of favourable odds, and heavily skewed positive outcomes. A simplistic view might be something like this:

A consideration many fail to think about is the following:

Although the dimensions for risk analysis could go on and on - risk takes on many different forms and outcomes are more often can be expressed in a range than in neatly constructed parameters.

Over time we can come to more easily recognise better and better opportunities, after having been exposed to both good and bad ones.

Learnings

In last year’s letter I lamented the following:

My results this year have been hampered by a large cash balance as I have scaled out of a few holdings, but also by not taking larger positions in new portfolio holdings.

This was a mistake I did not repeat this year. Whether it be luck, good timing, or serendipity, this year I juiced my opportunity set for all it was worth. That has certainly been the most gratifying thing, even though the results were also enjoyable. I am a much better investor and analyst than I was a few years ago, and that is really the important part.

They say no one bats .1000, but this year I got pretty damn close. Almost everything I sized up in worked. Almost everything that didn’t work was appropriately sized too. My longer term holdings went on tears, and reached stratospheric valuations. I enjoyed (personal) capital inflows at advantageous times which allowed me to reorientate the overall portfolio exposure in ways that derisked other positions without having to realise capital gains on positions which appreciated. As I mentioned before, the weakness of the Australian Dollar has been a boon. I got very, very lucky this year - and that fact is not lost on me.

As my portfolio became very concentrated in a single security in the middle half of the year, my focus narrowed considerably. This may have, regrettably, hampered the velocity of research and articles, but if my forbearance could bring more clarity to my readers in this regard then I think that was a reasonable trade off.

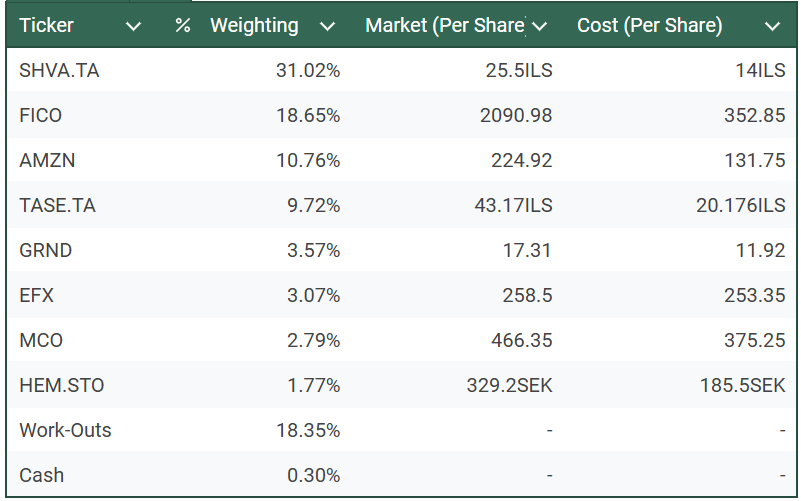

The portfolio as of the last update was:

The portfolio as it stands today:

The bigger moves I have taken in the last month or two has been dumping my smaller tracking position, starting a position in Equifax (article incoming, bear with me), and one additional work-out commitment which has been sized up. The latter, as a category, has been a good contributor to performance this year, although it has been absolutely dwarfed by the contribution of my longer term holdings. Generally speaking, I have been adding these to my portfolio when they arise, where the tax-adjusted IRR is acceptable, and when the risk on capital committed is low. As high quality businesses become pricier, I am looking to less conventional places for value.

In any event, so much of my overall performance going forward will now be reliant on a fairly illiquid Israeli payments infrastructure operator, which has seen recent business performance seriously inflect. As to my plan for 2025 - well I can definitively say there is no plan or strategy. As always I’ll hope to do my best to take advantage of opportunities as they arise. My continuing endeavour is to hold onto the companies that perform well at the business level (with only occasional reference to the price of their securities) and also continue to deploy their excess capital well. On the obverse, I look to sell when I am proven wrong in my assumptions, or when the company changes track for the worse at the business or capital deployment level.

Here’s hoping you have a wonderful end of the year with your family,

Larry.

Merry Christmas and a Happy New Year to you and your family Larry. Thanks for all the wonderful articles this year, I look forward to reading many more!