Dealing with Geopolitical Uncertainty

A (very) amateurish take on Israeli geopolitics and its consequences for SHVA and TASE

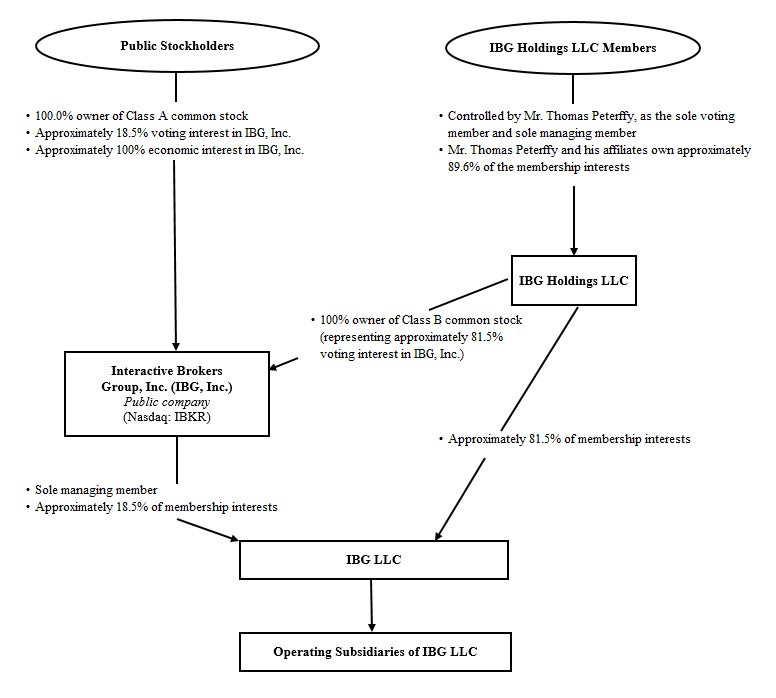

Firstly, a note on last week’s piece on Interactive Brokers IBKR 0.00%↑. There were several follow up comments and/or questions about IBKR’s ownership structure. As this is a bit complicated, which is already a bad sign, it’s a key consideration, and certainly worthy of follow up.

Interactive Brokers Group, Inc. ($IBKR) is technically a holding company that owns an 18.5% stake in IBG LLC (IBG), which currently operates an electronic brokerage business and formerly operated a market making operation. The remaining interest in IBG is owned by a management partnership. The largest individual interest in the management partnership is Chairman Thomas Peterffy.

When shares of IBKR became publicly traded (via a Dutch auction) they did so through an ‘Up-C’ IPO structure. The purpose of such a transaction is to preserve the tax advantages of a partnership when it decides to sell a portion of its business to the public. As mentioned, a management partnership remains intact (see below) as the original partnership did not transition into a more typical corporate structure.

You might need to read this a few times over. The management partnership - IBG Holdings LLC partnership - initially sold a 10% interest in IBG to the newly publicly listed corporation (IBKR) when shares became publicly traded. This interest has increased in the interim. The following infographic from IBKR explains

:

hnicalities aside, Peterfry controls the management partnership and hence also controls IBG LLC and its subsidiaries. The public equity of IBKR 0.00%↑ represents a minority interest in IBG LLC.

As a general rule, I like to own the same security as those who are exercising the rights of ownership, governance, and control. Opportunities for misalignment proliferate when this is not the case. Admittedly, IBKR’s history as a public company has not been punctuated by episodes of pilfering the minority interest. Quite the opposite in fact. The company has exercised regular and special dividends as well as opportune share repurchases. However, management’s approach to growing its capital base would likely not be possible without the control of a founder-CEO (now Chairman), who is free of the input of significant outside shareholders.

Whether or not that is a good thing, I’ll leave up to you.

Israel

Note: take the following with a grain of salt. Opinions vary widely into the motivations of the actors involved, and even the subject matter experts are regularly wrong in their analysis. This is simply my take - which has been informed by experts, as well as the public statements of the nation states.

While I’m loathed to comment on macroeconomics and the direction of factors extrinsic to a company (and hence outside of its control), seeing as there seems to be an escalation in tensions between Israel and Iran (and its proxies) - it seems a worthwhile exercise to walk through the events that have unfolded and the implications for both TASE and SHVA.

First things are first - hostilities commenced on October 7th 2023 when a number of Hamas and associated Palestinian militants crossed into southern Israel. Around 1,200 Israelis were killed, with more than 5,000 injured. Importantly, Hamas also abducted 253 Israelis, taking them back to the Gaza Strip.

Putting aside that Hamas’s raison d'etre is opposition to Israel, a key question is: why did they decide to attack Israel in this way and at this time? It’s important to remember that Gaza is entirely dependent on Israel for things like water, telecommunications, and a wide variety of other imports. For all intents and purposes, Gaza is an open air prison completely unable to sustain itself without external assistance. It represents one the most densely populated areas on the planet, with very little in the way of agriculture or industry. The unfolding of these events is even more puzzling when Israel’s response was obviously predictable ex-ante.

Most considered opinion seems to see a mix of factors contributing to this fateful decision. An amelioration of Hamas’s opposition to a two-state solution by the current leadership has been seen as undermining their internal legitimacy. This perception has been exacerbated by the fact that Hamas has let militant groups like Palestinian Islamic Jihad (PIJ) continue hostilities against Israel alone in recent years. On the other hand, it also shouldn’t be a surprise that Israel’s stance toward its Palestinian neighbours/cohabitants certainly hasn’t ameliorated either.

While I have mentioned Israeli demographics in broad terms in the past, what shouldn’t be underestimated is the ever growing influence of the religiously devout communities. Exempted from military service, taxation, and recipients of government payments, the ultra-orthodox devote a large portion of their life to the study of religious scripture. They also have very large families, early. What started as 500 families at Israel’s inception, is now 13.5% of the population. The birth-rate amongst ultra-orthodox women is north of 6.6 births per woman. Without delving too deep into Israeli politics, these demographic changes (amongst other important factors) have seen a succession of governments that have come to power by co-opting smaller, religiously conservative parties. The resultant policy has not been complimentary to the non-Jewish inhabitants of the West Bank and Gaza.

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.