Hemnet: 93% of the Way to Perfection (held)

Q1 24'

Hemnet reported Q1 24’ results last Tuesday. The similarities between the developing story of FICO 0.00%↑ (lastest note here) and $HEM.ST are striking.

First, the highlights as per the company’s update:

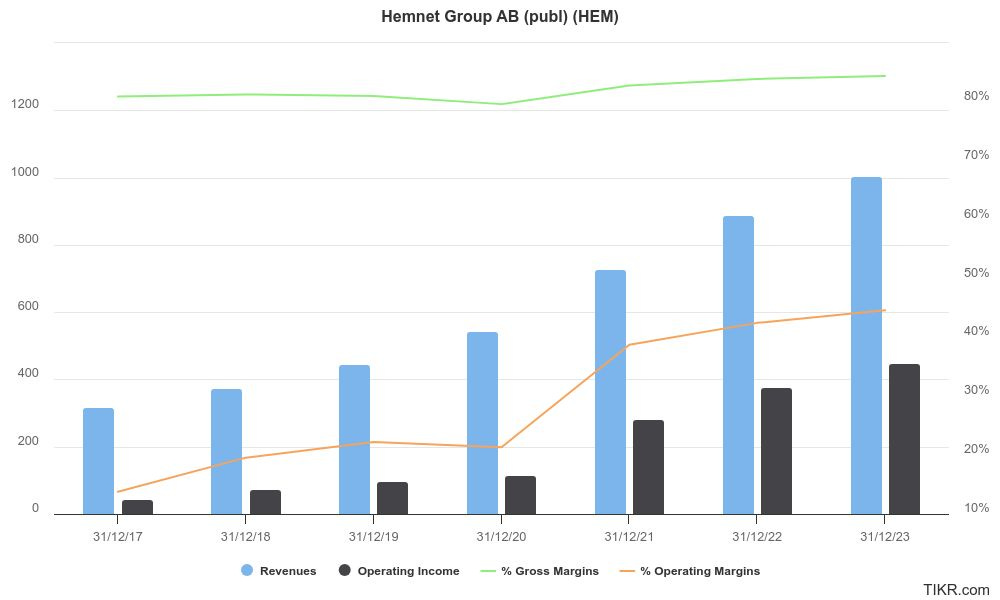

Net sales increased by 33.3 percent to SEK 253.4m (190.1)

EBITDA increased 37.3 percent to SEK 119.7m (87.2)

Operating profit increased 45.2 percent to SEK 98.9m (68.1)

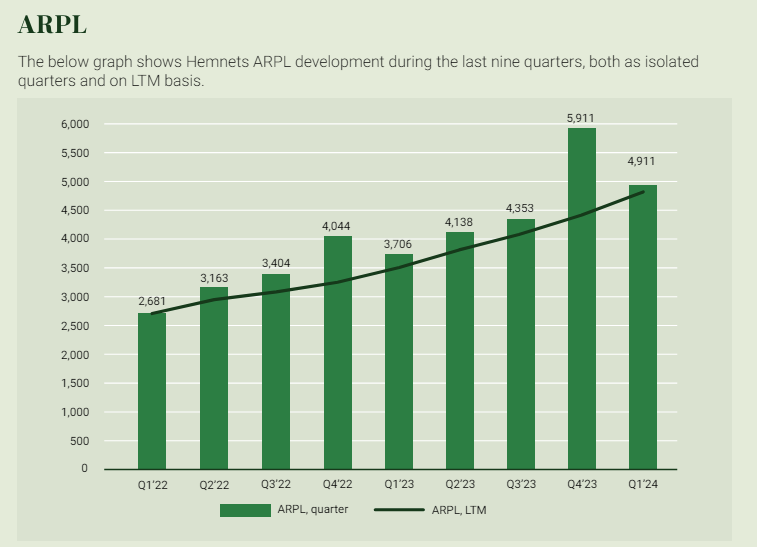

ARPL, average revenue per published listing, increased 32.5 percent to SEK 4,911 (3,706)

Fundamentally, these results are very, very strong.

I’ll rehash the context for those less familiar with the story so far. Hemnet was IPO’d via its private equity owner in 2021. As the dominant property portal in Sweden, its core advertising product (i.e. listing homes for sale) was both underdeveloped, and under-priced relative to its international peers. Since IPO, management has led an aggressive, if not straightforward, effort to commercialise the site - which has seen the price of listing a home for sale dramatically increase over the past couple of years:

Hemnet sits amongst the few businesses on the planet with enough pricing power to grow through almost any underlying market environment. Would it surprise you that during the 2022-2023 time period the volumes of home sales in Sweden decreased, peak-to-trough, over 20%?

The asset light nature of Hemnet’s business model, the predictability of its revenues, the sheer rate of growth, and its ability to return over 100% of free cash flow in buybacks and dividends has allowed it to command a premium valuation - on near term numbers anyway.

I am not Swedish, so I have found the reaction of local investors to the name somewhat puzzling. Hemnet’s perception amongst Swedes is one of near outright hostility, especially in the financial community. Case-in-point:

I think that’s what they call risk parity?

Most locals find the leading property portal in their geography to be obnoxious. These local networks tend to be very strong and their services are typically only available through the good offices of a real estate agent. For home sellers, having to spend money to reach buyers is naturally annoying. The ideal of home ownership is a proud one, and it hurts to find out that many other parties have a claim on the value of that ownership.

In any event, Hemnet’s economic characteristics are first rate. The rate of growth across every line item, as you can see above, is extra-normal. There are some local market dynamics which are noteworthy too. Like most peripheral Western markets, the truly quality names are few and far between. Most sharp local investors in these markets typically spend there time picking over a range of mediocre businesses, trying, in one way or another, to valuation arbitrage the more predictable names. Likewise, the retirement savings schemes in these geographies will often dwarf the fair value market opportunity of the locally listed publicly-traded securities. This is most acute in my home market, Australia, where the half a dozen or so legitimate quality names often trade north of 100x trailing earnings.

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.