Issue no. 18: Buffett's Notre Dame Lectures, Semiconductor Capital Equipment, Natural Monopolies

Issue no. 18: Buffett's Notre Dame Lectures, Semiconductor Capital Equipment, Natural Monopolies

Observations in value

Buffett's Notre Dame Lectures

I would say that almost everybody I know in Wall Street has had as many good ideas as I have, they just have a lot of [bad] ideas too - and I’m serious about that.

Buffett’s 1991 lectures at Notre Dame is some of the best reading I have done in a long time. For those interested, but uninitiated find the link here. The notes were taken by Whitney Tilson.

These snippets of Buffett from pre-2000, have been some of the most educational investing content I have come across. This includes the chapter of John Train’s Money Masters, the publicly available recordings of the Berkshire Hathaway meetings from the period, and now this.

These writings and recordings portray a man still at his intellectual peak. He didn’t have a capital base so large that it necessitated investments in capital heavy industries. Importantly, there isn’t the awkward question of legacy lingering around either that precludes the great man from speaking candidly; this is a period in his life where he was still taking large, concentrated swings in public equity markets.

Refreshingly, we also get Buffett expressing sincere beliefs as to what constitutes business quality. For examples, he couldn’t possibly get away with attributing his incredibly success to ‘pricing power’ in our current political climate.

Tests of a Good Business

A couple of fast test about how good a business is. First question is “how long does the management have to think before they decide to raise prices?” You’re looking at a marvellous business when you look in the mirror and say “mirror, mirror on the wall, how much should I charge for Coke this fall?” [And the mirror replies, “More”]

The consequently explained examples of a great business are Hershey’s and the Daily Racing Form. As an aside, Hershey’s is a 30-bagger in as many years since this lecture took place. The Daily Racing Form has a less glamorous ending (as has most of the newspaper industry), being reborn as part digital publication and part online betting app after a series of leveraged buyouts.

There are no surprises here. A franchise is almost defined by pricing power. It’s a tell that you have an in demand product with no clear substitute. This crucial element gives a firm control over it’s financial statements, and enables a business flexibility and resilience in difficult economic conditions.

Lord Thompson

Illustrating the differences between an excellent company, and an ‘agonising’ one, Buffett goes on to describe the business success of Lord Thompson (of Thompson Reuters):

Thomson Newspapers, which most of you have probably never heard of, actually owns about 5% of the newspapers in the United States. But they’re all small ones. And, as I said, it has no MBAs, no stock options – still doesn’t – and it made its owner, Lord Thompson one of the five wealthiest people on the planet. He wasn’t Lord Thompson when he started – he started with 1,500 bucks in North Bay, Ontario buying a little radio station but, when he got to be one of the five richest men, he became Lord Thompson. I met him one time in England as a matter of fact, in 1972, and went up to see him. He’d never heard of me, but he was a very important guy. (I’d heard of him!)

Here’s perhaps the genesis of the #neversell philosophy that has become a staple of Buffett’s investing regime:

I said, “Lord Thompson, you own the newspaper in Council Bluffs, Iowa. Council Bluffs is right across the river from Omaha, where I live, four or five miles from my house. I said, “Lord Thompson, You own the Council Bluffs [Daily Nonpareil?]. I don’t suppose you’d ever think of selling it?” He said “I wouldn’t think of it.”

Finally, Buffett describes the part of the exchange where Lord Thompson mentions how he prices his papers:

I said “Lord Thompson, you’ve bought this paper in Council Bluffs, and you’ve never seen the paper, never seen the town, but I do notice that every year you raise prices.”

He’s got the only way to talk to people – his was the only “megaphone” for merchants to announce commercial news in Council Bluffs. He said “I figured that out before you did.” I said, “If you ever raise prices to the point where it’s counterproductive.”

Then [I said] “I’ve got only one other question: How do you figure out how much to charge people? You look like a man of awesome commercial instincts – you started with a $1,500 radio station, now you’re worth $4 or $5 billion dollars.”

He said “Well, that’s another good question. I just tell my US managers to try and make 45% pretax and figure that’s not gouging.” And as I got to the elevator, he said “If you ever hear of a newspaper you don’t want to buy, call me. Collect.”

I rode down and that was two years of business school. I mean, try to make 45% and call me collect if you ever find a paper you don’t want to buy.

Characteristics of an Agonising Business

The phenomenal aspects of Lord Thompson’s excellent company (pricing power, which begets greater earnings, which begat more newspapers, etc etc) were contrasted against the mediocre American Telephone and Telegraph Company:

The telephone company, with the patents, the MBAs, the stock options, and everything else, had one problem, and that problem is illustrated by those figures on that lower left hand column. And those figures show the plant investment in the telephone business. That’s $47 billion, starting off with, growing to $99 billion over an eight or nine year period. More and more and more money had to be tossed in, in order to make these increased earnings, going from $2.2 billion to $5.6 billion.

So, they got more money, but you can get more money from a savings account if you keep adding money to it every year. The progress in earnings that the telephone company made was only achievable because they kept on shoving more money into the savings account and the truth was, under the conditions of the ‘70s, they were not getting paid commensurate with the amount of money that they had to shove into the pot, whereas Lord Thompson, once he bought the paper in Council Bluffs, never put another dime in. They just mailed money every year. And as they got more money, he bought more newspapers. And, in fact, he said it was going to say on his tombstone that he bought newspapers in order to make more money in order to buy more newspapers [and so on].

The idea was that, essentially, he raised prices and raised earnings there every year without having to put more capital into the business.

Therein lies our challenge with finding excellent companies.

Semiconductor Capital Equipment

After reviewing 21’/22’, it doesn’t seem at all ridiculous to say that these years were a bear market across a number of durable growth/quality businesses. The enormous rally in FICO 0.00%↑ shares seems to reflect this. Multi-year low multiples (which persist) in the likes of V 0.00%↑ and MA 0.00%↑ also seem to suggest this. Nowhere has this been as evident in the pricing in Semiconductor Capital Equipment shares.

These companies design and create the tools necessary to manufacture logic and memory computer chips. This is very obviously a growth area going forward. Advancements in IoT, auto manufacturing, AI, cloud computing, gaming, etc etc, all rely on every increasing amounts of compute to deliver bleeding edge applications and services. This trend has most recently manifested in the current craze over Artificial Intelligence - see the shares of NVDA 0.00%↑.

Firstly, let’s roll back to the idea of Gross Revenue Royalties - or the position of servicing capital intensive industries with capital light services. It appears to me (perhaps at too late a stage) that the semicap names express many of these qualities:

They are capital light and exceedingly efficient exhibiting outstanding ROEs and ROAs,

They set prices for their services - the capital intensive manufacturers of chips have constant capital expenditure needs. The semicap players own a royalty on this production,

Most have been constant share cannibals, and have paid constant dividends - as opposed to their customers who have had chequered capital return histories at best,

They sit within a rational pricing oligopoly, and each of the player serves relatively niche end markets which has made their businesses much less cyclical than the rest of their industry.

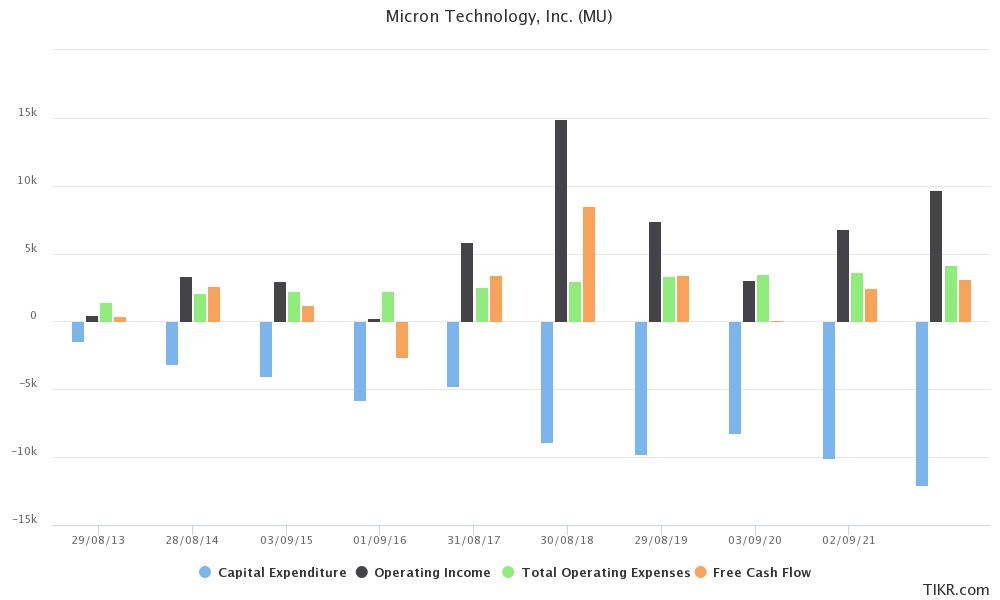

To illustrate the contrast in quality amongst chip manufacturers and capital equipment providers, let’s use a couple of examples. On one hand we have our agonising company - Micron Technologies MU 0.00%↑. Micron mainly competes in the manufacturing of memory chips (as opposed to logic), primarily NAND and DRAM. Some financials below to press home this point:

Despite what many onlookers have speculated at, the cyclical nature of the memory market persists despite the enormous tailwinds behind it. The volatile nature of this end market is set against a couple of unavoidable operating realities:

Capital investments march higher every couple of years, at a much more predictable rate than operating income may I add,

Operating expenses also march higher in much the same fashion, but are much more with management’s control.

The need for constant reinvestment, without much idea as to what the returns of those investments will be makes this a very mediocre business. Investment and cashflow cycles are also not set against each-other, increasing the risk that existing shareholders will be diluted in the firms insatiable need for financing.

Now for the excellent company - Lam Research LRCX 0.00%↑

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.