Issue No. 19: Channel Managers, The Fate of the New York Times, and Capital Allocation by Ham Sandwich ($BTI)

Issue No. 19: Channel Managers, The Fate of the New York Times, and Capital Allocation by Ham Sandwich ($BTI)

Lessons from early 2000's travel tech, great economics turned mediocre, and interesting capital allocation decisions

I work for a company (or at-least corporate entity) that basically created the ‘channel manager’ in Australia. This is a piece of technology that sits between a hotel’s (Operator) central reservation system (often referred to as a Property Management System - PMS), and that hotel’s listing on the large Online Travel Agents (OTA). Essentially, a channel manager ensures a constant updating (of nightly rates and inventory) between an Operator’s reservation calendar and their online distribution.

The value proposition of this tech is extremely straight forward: it’s incredibly time consuming and costly to manually update your OTA listings by hand. If you have tens or hundreds of rooms, this process could only be adequately completed by a team of reservation staff. In any event, you would eventually get double bookings (rooms booked twice or more for the same night), and rate disparities between different distribution channels. These are the absolute bane of the Operator’s existence.

Not to disclose too much information, and depending on who you believe, the tech was the brain child of a particular Gold Coast entrepreneur. He was, and still is, a hotelier and was acutely aware of how this particular problem was a significant opportunity in the market place.

While this particular paint point is always the way in which channel management gets sold (now either stand alone or as part of a PMS), the upside from adopting the tech is significant:

Greater number of bookings - both through having all rooms available for distribution,

Higher quality bookings - the ability to rate manage throughout the year sees greater yields for Operators,

Over time channel manager providers can overlay extra features which can have greater cost savings for Operators. An example of this would be an integrated booking engine available on the Operator’s website enabling direct bookings,

Less reservation staff needed for any particular property/number of properties.

While this is a now a commodity product, in the early 2000’s it was a genuine break through. It’s advent, and it’s consequent copying by well funded competitors, launched companies that are now worth hundred’s of millions of dollars. However, my company’s first mover advantage did not result in enormous fortunes - it resulted in a decently successful SMB.

So what happened?

I spoke to the long time CIO of the business yesterday (over a few cocktails admittedly), who made the point that while we made the initial breakthrough, and probably had the better tech for quite some time, it was the lack of an aggressively distribution strategy that saw others eat our proverbial lunch.

One of those competitors is a publicly listed firm called Siteminder ($SDR.AX).

Their go-to-market was, and still is, heavily based on personal sales. They also took the idea overseas, and targeted the large hotel chains who are the equivalent of this industry’s enterprise clients. Because channel managers don’t have a natural mode of distribution, and because the ticket amount is relatively low (average individual clients probably pay between $100-$300/month), the only method for expansion is investing in Sales and Marketing.

For a long time, and perhaps even now, this made sense. I have clients on our books who have been with us for over 10 years. The product is sticky because it’s such a pain to change, even though certain milestones like new management/owners is a catalyst for change. These switching costs infer limited pricing power (about 10% every four years from what I have seen). For the percentage of clients who will change, or go out of business, or who are starting new businesses (most commonly in the short term rental space - STR) it’s a fairly bitter battle between suppliers with very little differentiation apart from the commitment to sell.

Our company has always followed a kind of profitable growth model. Make money, invest it in staff and/or dev, rinse and repeat. This model only really makes sense in situations where you have a well defined competitive advantage. Software developers are often biased to think that superior technology is a legitimate advantage. Our CIO certainly does - and if you had spent your life building technology you would probably think so too. The reality is, of course, that competitive advantages are much more easily found in distribution, than they are in features.

The owners of the business are still largely bricks-and-mortar business owners, and the scars of previous internet business failures have enforced this mindset. The reality of the situation was that running at near term losses, which would have ultimately been investments, two decades ago would have seriously altered history, if not how the hotel industry operated online.

The Reality of Travel Technology

Outside of the Global Distribution Systems (GDS) that were pioneered decades ago for air travel, much of the online travel industry is about scaled advertising. The large OTAs are all massive scaled advertising machines. While their own particular contexts may have allowed them to scale efficiently, their market position’s today are enforced by their advertising budgets. Operators will always pay for bookings, but they won’t spend an iota of their time listing their properties on places where they don’t think they’ll get bookings.

This is why I have always thought that investors claiming that Booking.com or AirBnB are royalties on travel don’t really know what they are talking about. Scale begets scale, and (forgive the turn of phrase) the inventory isn’t loyal. This applies to the SaaS side of the equation equally. Having a genuinely successful software product that serves Operators relies almost exclusively on the ability of the provider to reinvest. If you look at Siteminder’s financials they have run at an accounting loss almost every year since their founding. I’m not sure what that means for shareholder’s long term, but these types of businesses can be successful if managed properly.

Winning at any moment in time, means simply winning the right to compete at the technological junction. In many cases, these markets are large enough for very decent businesses to be built, so it can make sense to invest over time. Sometimes they are just niche enough to really support only a few players. These are, however, not amazing businesses for shareholders. The software developers take their piece, sales take a piece, and whatever is left often needs to be spent again.

The Fate of the New York Times

I have written much about one of the great business modalities of the past: the local monopoly newspaper. The double occurrence of pricing power, and royalty like characteristics with many decades of profitable operation created many fortunes - including Buffett himself.

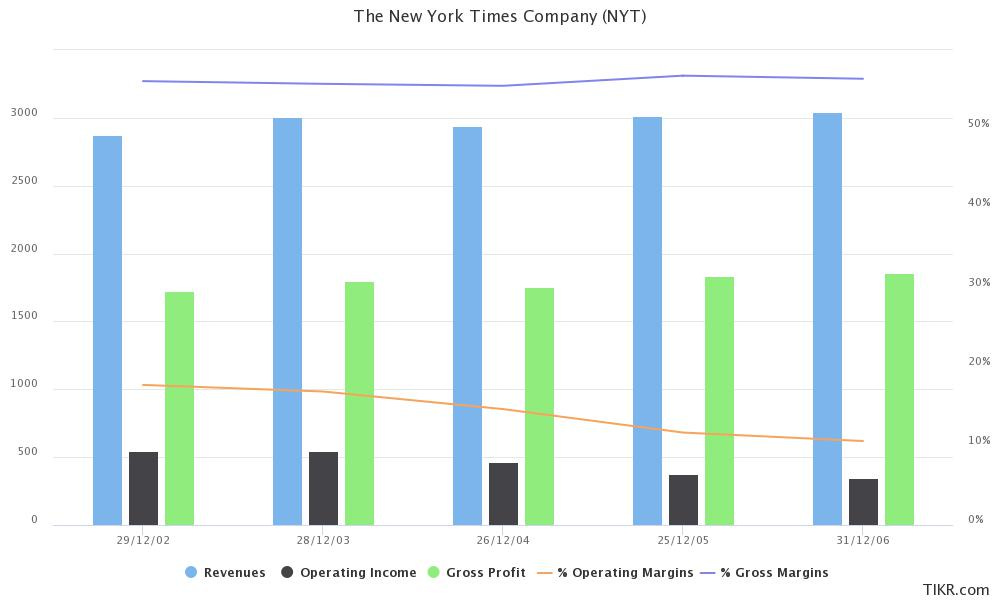

Since the advent of the Mosaic Browser and the consequent never ending march of the internet’s ability to distribute digital media, the newspaper generally has been in terminal decline. Apart from a number of publications with the brand name to scale online, many local issues have long since gone into abeyance. The New York Times Company NYT 0.00%↑ has been one of these properties who has bridged this gap. The story is informative.

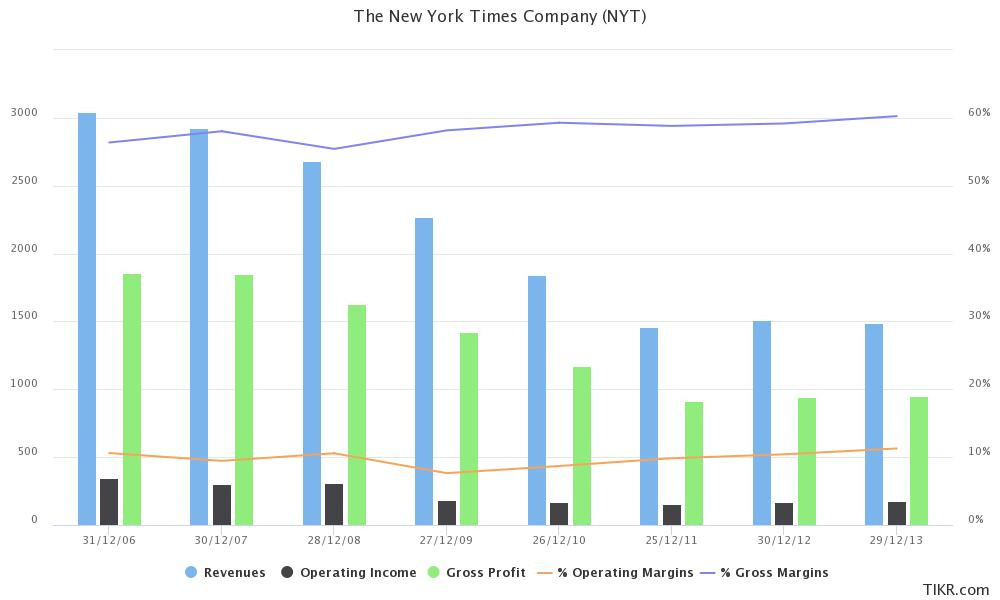

Even into the early 2000’s traditional newspapers were decently profitable. As you can see above this was in decline, but operating margins were still north of 20% into the turn of the century. Web 2.0 accelerated the general decline:

As Bucco tweeted earlier last month, 2014 was a watershed in the New York Times’ operations. The key challenge that faced these types of companies was clear: to succeed as an ongoing concern, traditional media companies had to find a way to transition to monetisation online.

This challenge is not to be underestimated. Traditional media, and specifically dominant newspapers, were one of the greatest modalities in history for generating cash. Importantly, this was not contingent on operational excellence. This was evidenced by the fact that so many dynasties operated profitably for decades. For the higher IQ operators (Murdoch, Packer, Buffett, Thompson), the act of reinvesting the cash proceeds into other newspapers created some of the world’s largest fortunes.

The internet, even in it’s vestigial state, offered the prospect of instant, free, and nearly limitless distribution. Overtime those eyeballs got gated by players with legitimate talent and innovative technology. Where newspaper proprietors once controlled the platform layer, they now became a minnow in someone else’s game. Journalism, or I guess we call it content creation, actually became the name of the game.

In 2014 NYT published an innovation summary which presented a path to digital transition. The piece starts with the following introduction:

The New York Times is winning at journalism. Of all the challenges facing a media company in the digital age, producing great journalism is the hardest. Our daily report is deep, broad, smart and engaging — and we’ve got a huge lead over the competition.

As the authors clearly outlines, differentiating oneself on the internet required legitimate operational excellence. Most of us who write know just how hard it is to capture lightening in a bottle - doing it everyday or every week is a gargantuan challenge. The quintessential business problem at play here is identified directly afterward:

At the same time, we are falling behind in a second critical area: the art and science of getting our journalism to readers. We have always cared about the reach and impact of our work, but we haven’t done enough to crack that code in the digital era.

On one hand, one needs to justify why a consumer would part with their hard earned dollars for information that is becoming commoditised. On the other hand, monetisation means subscribers or advertising - the newspapers of old could count on both.

So, a new strategy to grow readership was imagined:

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.