Issue No. 3: Making Sense of the Complex Vertically Integrated Monopoly

Issue No. 3: Making Sense of the Complex Vertically Integrated Monopoly

Inspired by the mental models of Sleep and Munger

In the last few weeks we have broadly discussed the ‘white whale’ of the business quality spectrum: a business so good that it needs virtually 0 capital to grow it’s earnings power. As I have stated, this is investing Nirvana. The problem with Nirvana, of course, is that so few people reach it.

If salvation is out of reach for most of the us, most of the time - these phenomenal franchises rarely go on sale - the only rational course of action is to find other escape mechanisms from investing purgatory. History, and general investing lore, shows us a way to the promised land: circumstances where returns accrue to scale.

This is an approach to business analysis that lends itself to traditional economic theory, as opposed to looking for those businesses which seem to defy it. If the prevailing wisdom is that a consumer acts ‘rationally’, it means that we can rely on her to ruthlessly shop based on price and need. Naturally, this explains why easily commoditised industries constantly fail to earn an economic return - however, sometimes these dynamics result in enormously successful enterprises.

This is worth exploring is some detail.

A note before we go deeper. The nature of this analysis is that it is both esoteric and narrative reliant. An intensive study of Bezos’s 1997 version of Amazon may have informed the next 1 or 2 years of financial performance. Amazingly, however, it would have been almost irrelevant in the context of what happened over the next 10 years. We can’t simply map out volumes, pricing, and assumed capital allocation.

In the few cases where an investor has identified one of these businesses and held onto it for a long time, the common approach seems to be: ‘it looked cheap when I bought it, and then I tried not to look at the share price again’.

If the lack of a formulaic approach here makes you uneasy, join the club. Insight is essential in this regard; to be without it is to fly blind. Culture, philosophy, and unusual historical circumstances all play into how some of these very large enterprises were built.

Nick Sleep’s Scale Economies Shared

Below will be a number of excerpts from the Nomad Investment Partnership’s Annual Letters authored by Nick Sleep:

In the office we have a white board on which we have listed the (very few) investment models that work and that we can understand. Costco is the best example we can find of one of them: scale efficiencies shared. Most companies pursue scale efficiencies, but few share them. It’s the sharing that makes the model so powerful. But in the centre of the model is a paradox: the company grows through giving more back.

Nomad Investment Partnership, Annual Letter (2004)

As stated, this general theory was key to thesis of Nomad’s significant 2002 investment into Costco (approximately 10% of assets at cost). From the outset, this approach requires an understanding of how the business operates at a fairly granular level:

Costco Wholesale is a member-only wholesaler of consumer goods. Membership is available to the public at a price of U$45 per annum. The act of purchasing membership has the effect of raising the company’s share of mind with the customer in the same way that consumer goods companies hope to achieve with conventional advertising. At Costco, the consumer has chosen to commit to the retailer. In other words, people shop at Costco because it is Costco, not because Costco stocks Coke.

For those of you who are up to date with their Cialdini, commitment and consistency bias is built into the essence of the shopping experience. Continuing:

[T]he reason they shop is that goods are priced at a fixed maximum 14% mark up over cost. The fixed mark-up is referred to in the industry as “everyday-low-pricing” or EDLP, in order to differentiate it from normal industry practice of changing prices in an attempt to influence traffic, or so-called high-low pricing. At Costco the consumer pays no more than 14% over what the company paid, period.

For a fairly modest annual membership, consumers get access to goods that the company has committed to pricing aggressively. This cost consciousness, by default, has to permeate the rest of the enterprise:

In order to make money at such low (gross) margins Costco must ensure that:

(1) Operating costs are low, indeed very low. It is indicative of the paranoia with which the company is run that costs are measured in basis points.

(2) That the wholesale price is as competitive as can be. The key to negotiating terms is that the number of items in a store (stock keeping units) are fixed at 4,000, and the right to fill one of these spaces is auctioned, with the supplier that provides the best value proposition to the consumer winning space on the shop floor!

(3) Revenues need to be very high. This last factor is partly a self-fulfilling prophesy – revenues will be high if the other factors, (1) and (2), are favorable.

To divert briefly, the above description also explains an episode in which a retired Jim Sinegal (former CEO of Costco) threatened to kill now CEO, then COO, W. Craig Jelinek over the price of the famous $1.50 hotdog:

For reference, the price has not been raised on the combo since 1985, and it sounds like Sinegal was not in favor of a change: “I came to (Jim Sinegal) once and I said, ‘Jim, we can’t sell this hot dog for a buck fifty," Jelineck recalled, according to a post by 425 Business. "We are losing our rear ends.’ And he said, ‘If you raise the effing hot dog, I will kill you. Figure it out.’ That’s all I really needed."

Delish article by Kristin Salaky

Needless to say, I have found it difficult to identify a theory of management that neatly explains this unique culture.

Resuming our analysis, the religion about costs creates a company exercising a cost advantage that is not easily replicable, even by very large operators:

This makes life difficult for Wal-Mart and the hypermarkets who cannot price at aggregate Costco levels and make money as their cost bases (approximately 15% and 25% of revenues respectively) are too high.

The key to negotiating terms is that the number of items in a store (stock keeping units) are fixed at 4,000, and the right to fill one of these spaces is auctioned, with the supplier that provides the best value proposition to the consumer winning space on the shop floor! Contrast this to normal industry practice whereby the supermarket assumes the role of landlord, auctions space to the highest bidder and pockets the rents (“slotting fees” in industry parlance). Many supermarkets make their money from buying from the supplier. Costco makes money from selling to the consumer.

The supplier relationships are unique. Costco negotiates long-term, exclusive contracts with their suppliers creating win-win outcomes for both parties. Once again, contrast this against the supermarkets, and *hushed tones* Amazon, who use their sales data to provide shoppers with lower cost products on popular SKUs.

The result for Costco is that they generate sales per square footage that appears abnormal in relation to their competitors. Scale begets efficiencies, efficiencies beget savings, savings beget lower prices for customers. Rinse and repeat.

The key to understanding this operating philosophy is that:

[A] firm is deferring profits today in order to extend the life of the franchise.

We’ll take another detour to deconstruct this:

The underlying assumption here is that ‘excess’ returns corrode the longevity of a business’s dominant market position. In most circumstances this is true. A derivative of this assumption is the understanding that if near term profits are being subordinated, much greater profits must exist in the future.

These future profits, which actually eventuated for Costco post facto, were a result of a replication of the model within and without the United States. At a certain scale, the membership model and fixed cost nature of the business exhibits operational leverage:

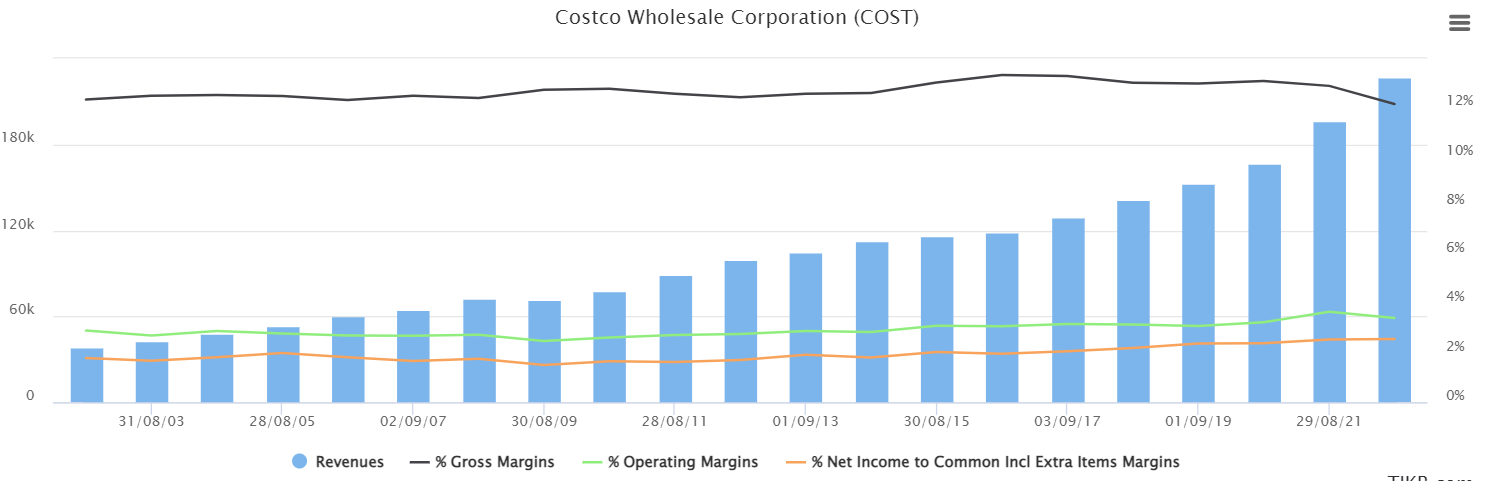

Operating and net income margins have (modestly) trended up over time, but even a few percentage points of incremental margin at their scale can be very accretive for the long term shareholder. If you call yourself a value investor take note - value is created between the margins.

Amazon, on the other hand, to the extent that it has been able to drive profits, has done so by raising their taxes on ecosystem constituents. On a secondary level, they benefit from operational leverage in both of their major business segments. This is obscured from time to time.

How did Sleep translate this into a valuation framework?

Heuristic Two: “it’s expensive at 24x earnings”. Really? Net income is a small residual, as discussed above. The firm could earn Wal-Mart margins by taking pricing up a little, in which case the firm would be on 11x earnings, but would it be a better business as a result?

My tongue-in-cheeck conclusion: normalise the earnings, and then determine whether or not the delta between reported earnings and underlying earnings power is making it a better business.

What could be easier?

‘The microeconomic advantages are largely advantages of scale: scale of market dominance, which can be a retailer that has advantages in terms of buying cheaper and enjoying higher sales per square foot… You can have scale of intelligence… so by and large you are talking about advantages of scale and low agency costs’

Charlie Munger, Berkshire Hathaway Annual Meeting (1995)

Munger is well known for his adoration of Costco. His brief public contributions on the nature of the company reassert the essence of Sleep’s conclusion: through a bizarre mix of management culture and their unusual business model, the company enjoy’s a unique cost advantage.

I’ll be bold here and add my own observation. Simply deferring profits now to extend the life of business, in a vacuum, is a recipe for a permanent mediocrity in returns to capital. What makes the model work is the spectre of two outcomes:

Operational leverage - this is certainly the case in the case of Costco, Amazon, and a number of Berkshire Hathaway businesses (like GEICO),

Significant secular growth - many commodity companies often exhibit characteristics explained above, but lack the reinvestment opportunities that bring returns to scale.

The corollary to this point is that actual capital returns are subordinated to reinvestment in the defence and enhancement of a cost advantage.

That’s all for this week’s Issue, as always remember to subscribe if you havn’’t already to keep up with the journey.

Be sure to checkout my trusted, used, and Buyback approved financial tools below. I only promote products I personally pay for, and find value added:

TIKR Terminal - for all of your historical financial information publicly listed securities. A Bloomberg terminal for a great price.

Trading View - useful for all your charting, news updates, and historical dividend and corporate action needs.

Warren Buffett Jokes About Charlie Munger's Costco Obsession https://www.youtube.com/watch?v=Z1sTs8wkAbw