Passing on Equifax Pt. 1 - The glory of The Work Number (TWN)

Passing on Equifax Pt. 1 - The glory of The Work Number (TWN)

A great asset

Equifax is pretty squarely in my wheelhouse. The credit bureaus (CB) sit within the same financial ecosystem as FICO - in many ways they are in a symbiotic relationship. When you study one, you pretty much have to study the other.

The CBs - that is to say Equifax, TransUnion, and Experian - have been extensively well covered in the wider financial ether. They constitute a natural oligopoly in an industry that has been consolidating for almost 50 years, and has existed for over a century. These are good businesses, although perhaps not great businesses.

As a stand alone proposition, the CBs are not that interesting. Industry consolidation has naturally been good for the economics of a CB, but the extent of this consolidation has also muted the wider growth opportunity. In the US they are well into their mature phase of operation. While there is some pricing power, they are not in the early innings of it. Alarmingly, there are also significant threats to their competitive positioning - as of this writing the Federal Housing Finance Agency (FHFA) has handed down rulings that are explicitly aimed at introducing pricing competition amongst the players with respect to mortgage. This is a present and imminent danger.

As I spoke about with a friend recently, I’ll take the tax on top of the tax on top of the borrowing public - that is to say: if I already own the best business in this particular value chain, why own a weaker part?

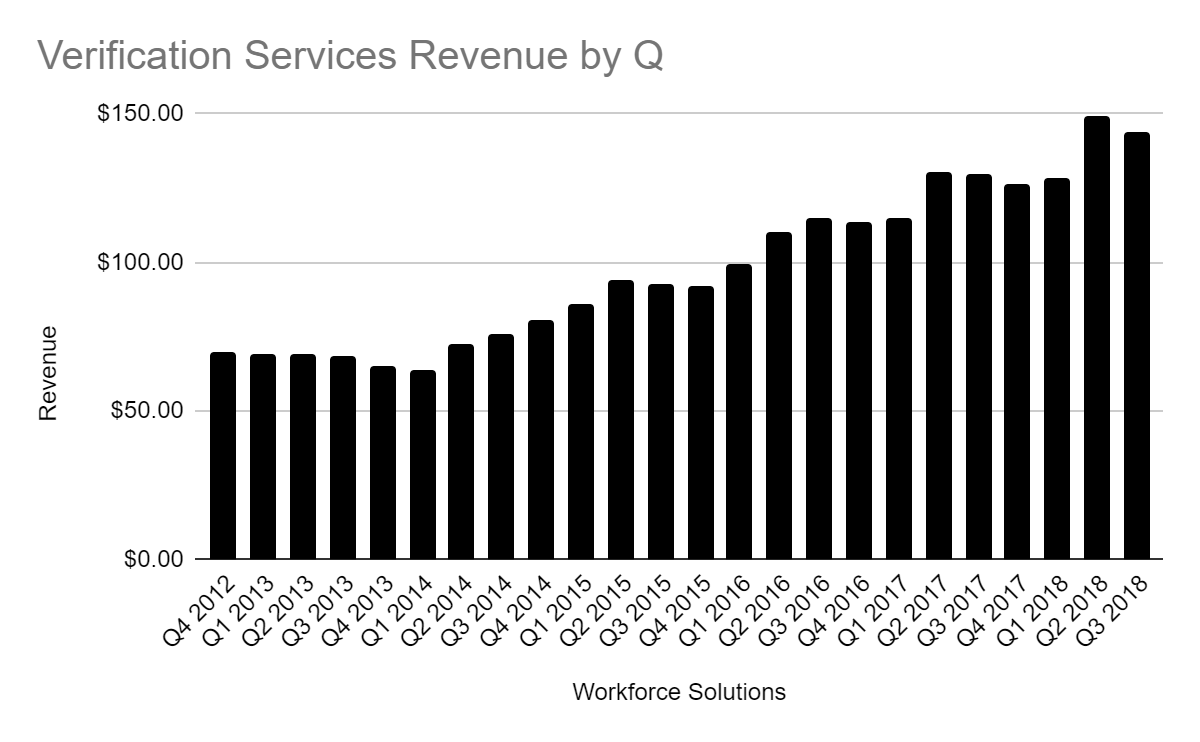

Of course what made Equifax peak my interest wasn’t anything to do with the CB part of the business - which has some significant issues independent of those already mentioned - it was The Work Number (TWN)…

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.