The Weekly Investing Digest (06/02/2023)

The Weekly Investing Digest (06/02/2023)

Interesting investing resources from a week in the fintwit pits

We’re deep in earnings season, so my focus this week will be less philosophy and more analysis. Apologies in advance if you were hoping for media - Sermon and Mantra become one this week: ‘Simplicity’.

As I have learnt the hard way, complexity, in all of it’s forms, corrodes natural judgement and heightens uncertainty. The best ideas are almost always easy to explain, both in the qualitative narrative explanation, and in the quantitative reasoning. In the Grahamian approach to deep value, it’s as easy to explain as it is to observe that a security trading for less than it’s working capital is attractive. One doesn’t need extensive mathematical training to know that purchasing dollars for fifty-cents is a compelling proposition.

Yet the eighth deadly sin is complexity - man seems forever doomed to make his life more complex than necessary. No where is this more true than in his investments.

Once again, this is an area of life where the wisdom of Buffett stands out. Remember that this is a man who has lived in the same upper middle class home his whole life, has had the same daily routine for over ~60 years, and irrespective of his unusual domestic arrangements, had the same friends for many decades. He’s fond of the quote:

Everything should be made as simple as possible, but not simpler.

Albert Einstein

He’s also found of saying:

I don't try to jump over 7-foot hurdles: I look for 1-foot hurdles that I can step over.

Personally, I’m partial to the puritanical simplicity of Pascal:

All of humanity's problems stem from man's inability to sit quietly in a room alone,

Blaise Pascal

The things which plague any human’s ability to properly analyse investments is of course complexity, although we like to dress this observation up too. This phenomena is conveyed as thesis drift, re-underwriting, or the dreaded reliance on a #neversell mentality when we are stumped for answers. I think a bit of self reflection is in order here, and with the zealotry of a convert, I’ll compare the quarterly results of two companies I own as contrition.

The first company, which I will uphold as the epitome of simplicity, is Fair Isaac Corporation. Even though it’s software segment seems to be developing satisfactorily, I will focus on it’s consumer credit scoring business - which enjoys a duopoly market position, and requires virtually no capital to grow. Pricing power, and it’s irreplaceable, what could be simpler?

On the other hand I have the complex-virtually-integrated-type-business Amazon. It would take about 9 hours to explain everything the company does. Broadly, it offers a suite of eCommerce services in North America underpinned by it’s Prime programme, it offers eCommerce services Internationally (where it has not been as successful), and it offers Infrastructure-as-a-Service globally through Amazon Web Services (AWS). As I write this, I’m lashing myself for how many brain cells I have lost trying to understand the business holistically.

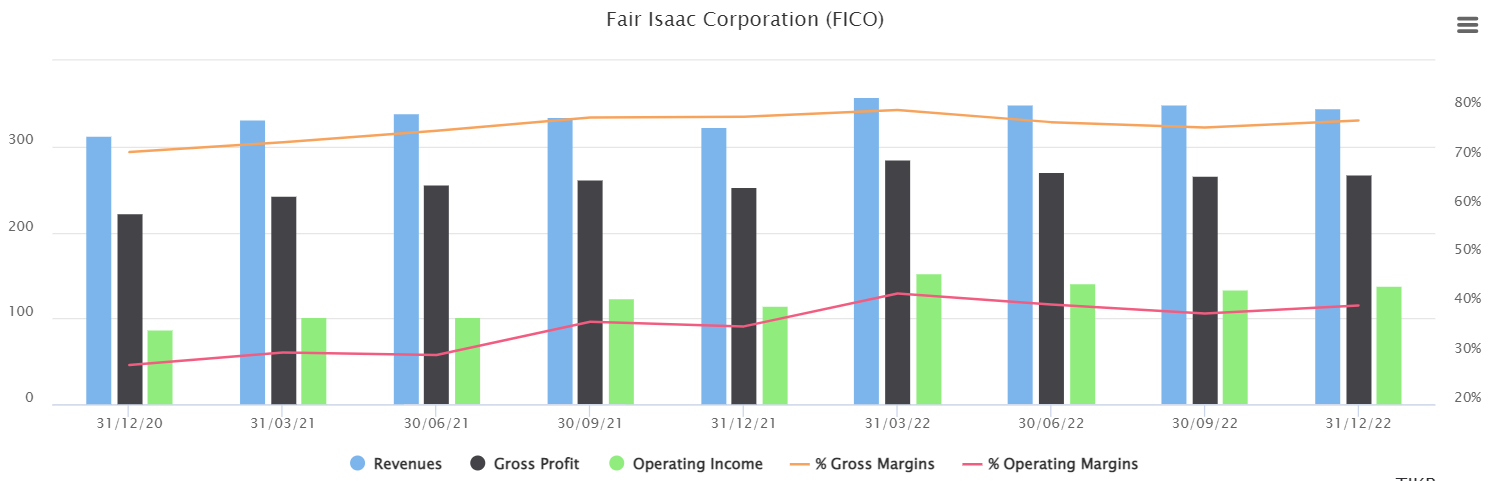

Using my trusty TIKR Terminal I can analyse the last 8 quarters of financial results of Fair Isaac Corporation with ease:

Hmm, revenue, gross profit and margins, and operating income and margins all up and to the right. No head scratcher’s there.

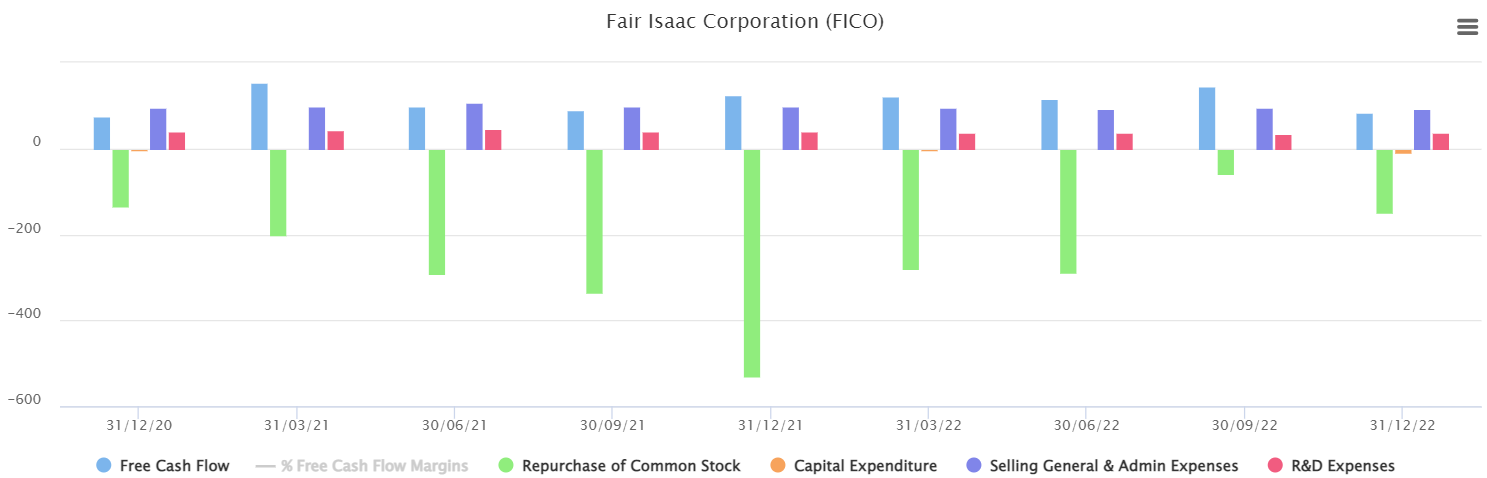

Good FCF conversion, capex isn’t even visible, SG&A kept steady over the past two years despite the lax environment in the capital markets generally. Oh, and they are retiring shares like it’s going out of fashion. Leveraging the balance sheet to repurchase shares can make sense under the right conditions, and I know that the majority of the debt taken on by the company is fixed at around 4.9%. Not a bad deal for a company with a long lived franchise and strong underlying earnings growth. Q4 2022 was simply more of the same. I can go back to doom-scrolling Twitter knowing my capital is well stewarded here.

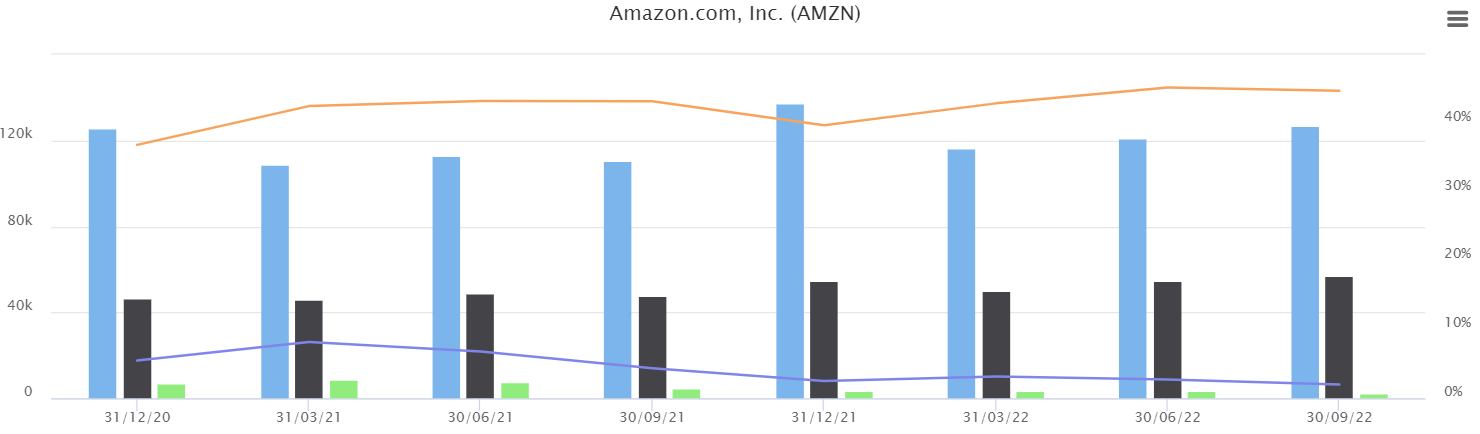

And now Amazon:

There’s a good degree of cyclicality in the quarterly headline financial numbers - the large retail business (a good portion of which is low margin 1P products) both accentuates top line numbers and compresses margins in the 4th quarter annually. Outside of the Christmas Holiday quarter, margins rebound as the higher margin business lines make up more of the overall revenue. Operating income has been steadily trending downwards, due to the immense investments made during COVID, massive over-hiring, and the inflationary pressures affecting prices generally. Not the worst thing I have ever seen, but nothing to write home about either. Investing in the company now is believing that the operating results will meaningfully inflect in the coming years.

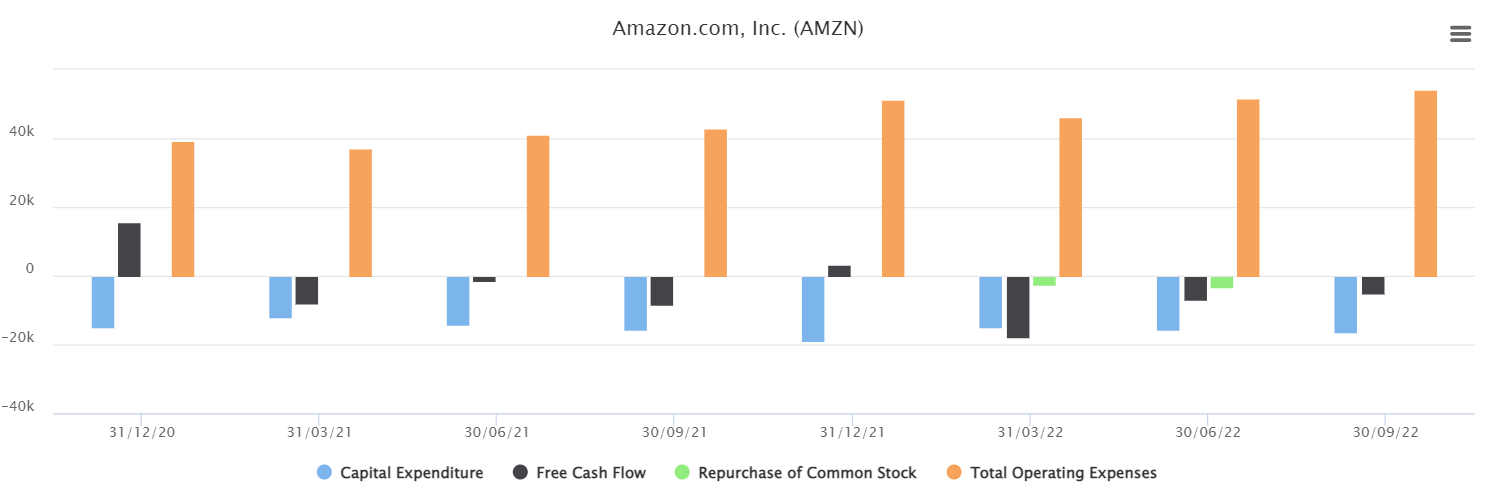

The other side of ledger gives us an even more gruesome picture. Growing operating expenses and capex, coupled with very poor, often negative, free cash flow numbers. This time around the share repurchases are almost imperceptible. Again, these factors add significant complexity to evaluating the company.

As a sophisticated and interested person, you will probably know that this is taking Amazon’s operating results to a level of simplicity that doesn’t really paint a true picture of what’s really going on. Let me explain.

The eCommerce segment of Amazon’s business can broadly be broken down into North America and International. Amazon’s oldest international markets are in Europe (most prominently the United Kingdom and Germany). However, they operate in a vast number of international markets. The common characteristic that ties these geographies together is that they are unprofitable for Amazon to operate in. Explaining the nuances of individual markets isn’t worth either of our time - suffice to say that the North America consumer is the most profitable in the world both because of the services they demand and are able to pay for. The North American continent is easily traversable, and has more than adequate infrastructure to facilitate efficient commerce.

The NA eCommerce business has been modestly been profitable over time. It sits at a historical crossroad - a huge infrastructure and logistics build out contrasted against an ever greater ability to monetise 3P merchants and their Prime subscribers. Under the hood, they have a quickly growing advertising business (a combination of monetising 3P merchants and adding an ad load to their digital platforms), and a equally healthy 3P merchant business. This is at a time when their 1P eCommerce business is experiencing maturation (or even decline) as they decide to scale out of it. Complex - but we’re not done yet.

It is generally observed that the majority of Amazon’s market value is reflected in their Web Services business. Without getting too technical, this a is a service that allows digital businesses to turn the fixed cost of renting or building out data centre infrastructure into a variable cost. This is one of those few businesses that requires mind boggling scale to operate profitably. Only a handful of internet companies could of had the scale to even think about competing in this market and, outside of China, 3 players make up the vast majority of the market. It has the spectre of operational leverage, but it does go through intermittent investment cycles due to the required physical infrastructure.

Input costs, investment cycles, and growth rates aren’t easily modelled so the operating performance of AWS has been somewhat volatile over time, although solidly profitable. AWS is in the awkward position of being a service provider to a number of businesses that Amazon competes directly with in other fields. Netflix was an outspoken AWS proponent in the early days of migration to the cloud. How does Amazon repay that kind of loyalty? By competing directly with them in streaming (sequencing entertainment markets not withstanding). OK - we’re onto paragraph 7 now, and I’m not even close to giving this company a proper over view.

Amazon also has a slew of start up investments and emerging business lines which covers everything from self driving cars, to walk out technology in grocery stores. Thankfully, these are inconsequential so I’ll save my brain cells by resisting the urge to delve deeper here.

The bottom line is that Amazon is hosting both a ballet recital and warehouse-doof at the same time. It’s not that simple to analyse what’s going on. This is an X amount of Capital x ROIC calculation - investors are hoping that the large investments that are taking place will result in meaningful financial performance over time. Complex, nuanced, and insight needed.

If these brief narratives weren’t enough to illustrate the point I’m trying to make here, perhaps a few quotes from management can mail the point home.

Will Lansing, CEO of Fair Isaac Corporation, summarises the scores quarterly results in two paragraphs:

In Scores, revenues were up 5% over the same period last year, as you can see on Page 6 of the presentation. B2B revenues were up 11% in the quarter versus the prior year, driven by unit price increases, increased volumes in card and personal loan originations, and also by a license renewal in Latin America.

Our B2C revenues were down 6% versus the prior year quarter as we continue to see difficult comps in our myFICO business due to the economic climate and especially because of the higher interest rates and lower number of consumers preparing for mortgages.

It’s pretty self explanatory.

Amazon, on the other hand, naturally has to turn their investor call into a quasi-marketing spiel. They do this for the simple reason that the myriad of business lines make even a curt overall explanation a time intensive event. For some reason they spent valuable time talking about the Lord of the Rings prequel series, despite it’s well known mediocrity in terms of generating Prime Subscriptions.

OK, you get the point. A simple business that delivers more and more capital to it’s owners every year, with no great need for reinvestment (and hence strain our ability to evaluate those internal investments) is really investing nirvana. It might also surprise you that Fair Isaac Corporation has outperformed Amazon in share price performance since late 08’ - and they didn’t even need to create the world’s most profitable technical tech company to do it.

Be sure to checkout my trusted, used, and Buyback approved financial tools below. I only promote products I personally pay for, and find value added:

TIKR Terminal - for all of your historical financial information publicly listed securities. A Bloomberg terminal for a great price.

Trading View - useful for all your charting, news updates, and historical dividend and corporate action needs.