The Weekly Investing Digest (for the week of 13/2/2023) - $GOOG

The Weekly Investing Digest (for the week of 13/2/2023) - $GOOG

Interesting investing resources from a week in the fintwit pits

Despite my best efforts to the contrary, this week my investing resources have been consumed by the ChatGPT-Bing-Google affair. When Harold McMillan was asked: ‘What is the greatest challenge to a statesman?’ - he replied: ‘Events, dear boy, events’. As investors, the challenges we face are one in the same.

In Shakespeare’s Henry the Sixth, English noble houses pick between the red and white roses at the Temple Garden to indicate their support for the houses of Lancaster or York in an imminent civil war. So too, in regards to this latest episode, has the media and fintwit-at-large been nailing their colours to the mast. The gauntlet has been laid, and a challenge declared.

For those uninformed about the momentous events at hand, a short summary is in order. OpenAI, an American artificial intelligence laboratory, released a publicly available chatbot called ChatGPT on the 30th of November 2022. This was followed by general media fanfare, and great memes, as users found the long form text responses to their questions intelligible, efficient, and in many cases good enough to perform their own jobs.

Fast forward 3 weeks, and Microsoft announced a $10B investment in OpenAI, on terms that would make Tony Soprano blush. On the 7th of February - six days ago as of the writing of this article - Microsoft announced the re-invigoration of their Bing search product, now augmented by a chat function that can generate it’s own content, and long form answers a la ChatGPT. This announcement was coupled by a concerted media campaign by Microsoft CEO Satya Nadella, essentially declaring war on Alphabet:

From now on, the [gross margin] of search is going to drop forever… There is such margin in search, which for us is incremental. For Google it’s not, they have to defend it all.

Satya Nadella, Financial Times

This threat was compounded with some good old fashioned blustering and bravado, reminiscent of a previous Microsoft CEO:

This new Bing will make Google come out and dance, and I want people to know that we made them dance.

Google came back swinging with the unveiling of their own chat product called Bard, which acrimoniously returned false information during it’s demo earlier this week. The market capitalisation of Alphabet is off about 12% since Wednesday morning.

And so, the War of the Digital Roses has begun.

A personal disclosures before we continue. I am an Alphabet shareholder, and have been so since March 2020. It is a large position in my personal account. I have not purchased any shares since 2020.

Generally speaking, I am of the Druckenmiller persuasion, although I am less sanguine on the quality of management than the quality of the enterprise. Google search is a phenomenal business: a gatekeeper (and hence toll collector) to being discovered on the internet with operational leverage. Alphabet’s other significant properties are impressive. Everyone reading this article is probably doing so on a Chrome browser, has watched YouTube today, and uses a software product supported by Google Cloud.

The last decade has seen the business go from strength to strength while the core search product has continued to draw vast economic rents. Google search, as a product, has subtle competitive advantages and in a vacuum is subject to the same kind of UI/X and platform risks that Facebook faces.

Google’s strategy has been to vertically integrate search from the platform layer up. This was prescient - but it wasn’t easy. Building the dominant browser product, developing properties like Gmail, YouTube, and G Drive/Suite to slowly extract personal information from users was a touch-and-go process. Now many of us are locked into the greater ecosystem, and changing certain online experiences would now be extremely painful.

Furthermore, the company pays vast sums to Apple to be the default search product on iOS, an arrangement that benefits both firms. More on this later; it informs where Alphabet may be heading.

Microsoft’s challenge presents a serious, if not an existential, question for the company. At the risk of reinforcing my own biases, I’ll present a future for Alphabet that should be satisfactory for the current/marginal investor.

The essential question at hand is the significance of the spectre of LLMs generating content that will supersede search’s current medium of returning indexed web-page results. Two very clear implications standout from the dynamic:

(1). Currently, generating content ChatGPT-style is much more expensive from a computing standpoint. Internal Google employees indicate that if Google were to roll out such a function en masse, it would seriously impair the enterprise financially,

(2). It is likely that longer-form self-generated content responses monetise less well than traditional search.

From a first principles stand point, an investor needs to make a judgement on how charismatic this new age of AI powered search is. It has certainly captured the imagination of the VC, investing, and media community. The early, and loud, proponents probably honour this new innovation more in the breach than in the observance. For reference, ChatGPT has very proudly promoted their user growth numbers- and they are spectacular - they haven’t, however, been as promotional with their churn rates.

The second question is a derivative of the first: how much of traditional search will get cannibalised by these new chat-like features?

It’s far too early to make any kind of sweeping judgements. However, any change in the steady state status quo is a net-negative for Google’s gross margins - the future growth rates and operational margins are less certain.

A few tweets I thought were insightful:

Ben expands on his point:

Even though this idea was presented tongue-in-cheek, it harkens back to Ben Thompson’s Aggregator Theory. Search is a time saver, not a time black hole. It doesn’t derive value from hijacking a lower brain function; it derives value from offering users much greater value than it extracts from them. Innovations that increase the delta between extraction and value is positive-sum commercially and philosophically.

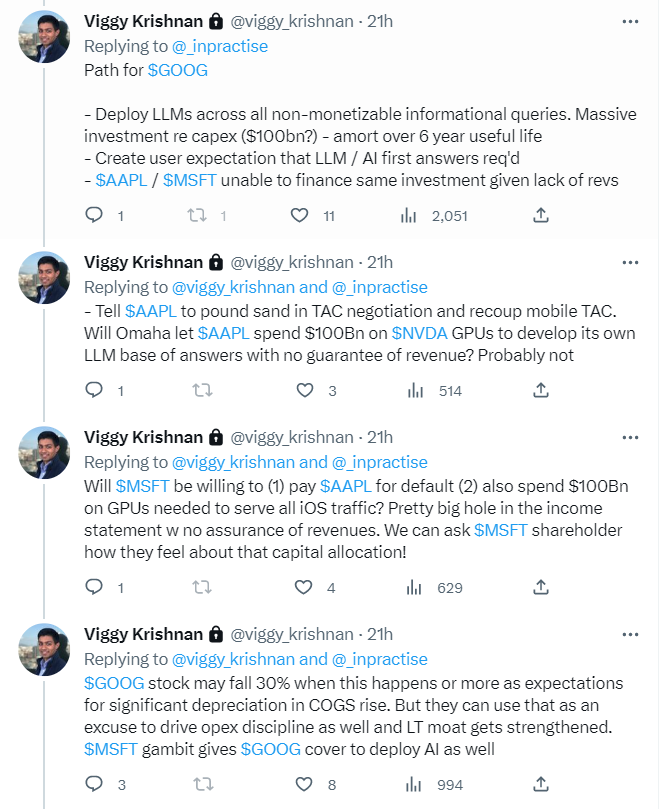

Viggy Krishnan:

The playbook presented by Viggy is a kind of judo-like response to Nadella’s margin threat: make the bar to play in search prohibitively high. For reference, Google monetises something like 20% of all search results - meaning there’s considerable space for change that won’t affect monetisation. The question of costs is different.

What the market still fails to appreciate is how much progress this company can make below the gross margins. Microsoft can pursue pie-in-the-sky unlimited TAM projects in search to their heart’s content - it doesn’t change the fact that Alphabet can catalyse immense cost savings in their OpEx (of which we are seeing the beginning), and there can be a sea change in the company’s approach to capital allocation.

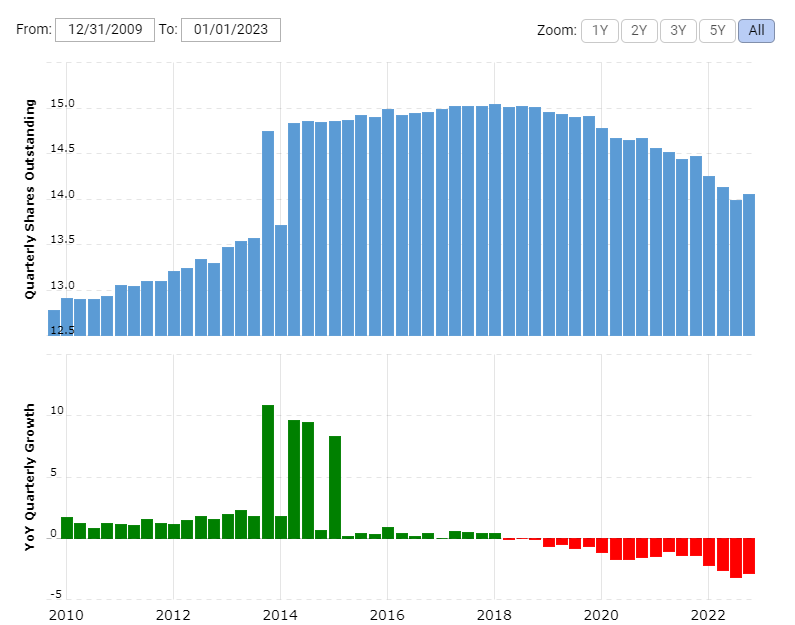

For example, every year the company authorises a larger and larger share repurchase program, that has seen shares outstanding decline at a greater and greater rate YoY. While terminating excess employees will have significant one-off charges, eventually this would also result in less of a SBC drag on an investor’s TSR. As this plays out the cash balance can be run down - at a certain stage the company may choose to lever the balance sheet to retire shares opportunistically.

The destination of the company’s current trajectory is a model of better operating results, and steadier EPS growth despite a lack of 15-20%+ revenue growth. I think we can all assume the latter is a thing of the past, especially at this kind of scale. Even more to the point, this is a recipe for solid shareholder returns as verified by history. Visa, Apple, FICO, Moody’s, and Verisign all follow a similar formula, with spectacular historical results.

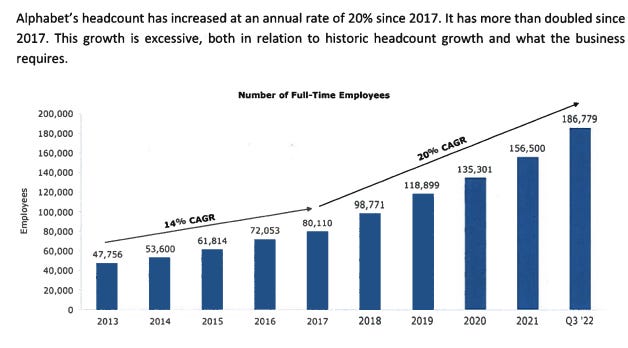

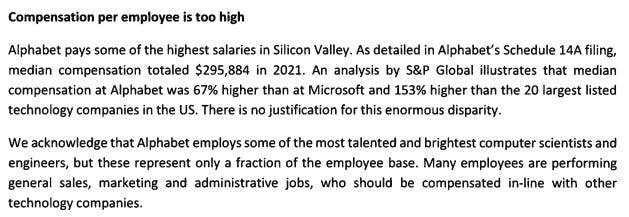

For those of you blissfully unaware of Alphabet’s, ah uhum, less than stellar discipline in their operational expenses, let me expand using several excerpts from TCI’s Chris Hohn who authored a letter to the company last November:

Now for the really good stuff:

Hohn owns a percentage of the company in the high single digits, and this piece was the catalyst for a substantial reduction in headcount during December and January. Management’s language has changed somewhat in the last quarter, but remains strategically ambiguous.

What remains, irrespective of any perceived competitive threats, are significant value accretive levers exclusively within management’s prerogative. Having said this, I’m not convinced at all that Google has even been wounded yet - advertising headwinds and general macro concerns not withstanding. To illustrate the climate of mis-sequencing history in the current prevalent narrative:

This observation is categorically untrue. Google competed with Facebook in social, Microsoft and Google competed with Amazon in cloud, Shopify competed with Amazon in eCommerce, Google competed with Microsoft in core Office products, and they all competed with Apple in hardware - the list could go on endlessly.

The truth is that tech has (please observe the tense) been a place where great monopolies have been formed. These key domains have been larger and more durable than most people have thought possible. The question for the next decade is if that remains true.

That’s all for The Weekly Investing Digest, as always remember to subscribe if you haven’t already to keep up with the journey.

Be sure to checkout my trusted, used, and Buyback approved financial tools below. I only promote products I personally pay for, and find value added:

TIKR Terminal - for all of your historical financial information publicly listed securities. A Bloomberg terminal for a great price.

Trading View - useful for all your charting, news updates, and historical dividend and corporate action needs.

Viggy's point hits the nail on the head, "make the bar to play in search prohibitively high." The very same point I made in my Meta piece The Zuckerberg Flop, "Every inch the bar is raised translates to substantial incremental returns for Meta and competitors losing share." While nothing is out of the question, it wouldn't surprise me to see the 'inappropriate levels of reinvestment' occurring at other large tech firms to yield similar results. Perhaps through the lens of hindsight they will begin to look quite appropriate.

Another fantastic piece, I really enjoy your writing. The new OID! I have to say I’m in camp Google on this one. People have integrated the google account into their everyday lives. Maps, reviews, YouTube, Gmail. Furthermore, I don’t think the average searcher even cares/knows about Chat based search, they just want to find what they are looking for quickly. Not to say that won’t change over time but I think the search moat is secure for the next decade UNLESS apple expands their iPhone spotlight feature to include a search engine.