The Weekly Investing Digest (for the week of 5/3/2023) - $CRM and The Base Rate Book

The Weekly Investing Digest (for the week of 5/3/2023) - $CRM and The Base Rate Book

Investing Resources from a Week in the Fintwit Pits

I’ll start this week reflecting on a previous position I had in the portfolio under somewhat reluctant circumstances. I’ll let Pythia open the discussion:

CRM 0.00%↑ reported earnings this week, and impressed investors with their ability to change, on a dime, their entire operating ethos. After years of enormous acquisitions, and a religious devotion to top line revenue growth, CEO Marc Benioff is now worshipping at the alter of operating income margins, and heavily adjusted EBITDA numbers.

Personally, I owned the shares for a short period of time post Salesforce’s acquisition of Slack. While I was quite excited about getting an instant 50% re-rate in the quoted price of my Slack shares, I was far less excited by the prospect of owning Salesforce. In many ways Salesforce is the inverse Slack.

I have written ad nauseam about my love for Slack, and my belief in Stewart Butterfield as a CEO. If you’d like to get a quick run down on my thoughts at the time, and after the investment, click here and here. However, Slack was a genuinely innovative company that was led by a visionary founder-CEO. Virtually all Glassdoor reviews on the company were overwhelmingly positive. The culture of the company was genuine and organic. The main executives were clearly very intelligent, and deeply invested in their mission. Even though it sounds a little cheesy, Slack was a product that was so good it sold itself - in retrospect this approach was a mistake, but you get the point.

Salesforce, while it was an innovative product at its inception, is not that intuitive, and genuinely frustrating to use. This is also quite a bullish point for them - when the product is genuinely difficult to use yet customers still implement it en masse, you’re really onto something. The recent history of the company has seen them aggressively invest in sales and marketing to drive top line growth at all costs. It has also seen them make a number of progressively large acquisitions with somewhat middling results after the fact. Benioff has also churned through a number of potential successors, all the while personally selling stock at every opportunity. The hyped up sales culture (ahem “Ohana”) seems completely contrived - and one gets the feeling that no genuine technology people work there. Having dealt with a number of staff there, I can attest to the point.

The climate of easy money post-GFC supported an ever appreciating stock price at a plus 10x sales multiple. Considerations about cost efficiencies, discipline in headcount, and being able to flex the operating leverage promised by a genuinely successful SaaS business were all but forgotten. Until last week it seems.

Pythia illustrates two points that I have come to appreciate about investing generally. Firstly, expecting turn arounds to turn around is usually a waste of time. If you can assess management’s track record, and they communicate their strategy before hand, you can reasonably expect them to continue down that road. If, on the other hand, you expect management to change track and for that track to conveniently mimic your desired strategy, you’re going to be disappointed.

Secondly, it’s best to avoid low return on brain damage investments. This is why Buffett and others stress simplicity in their investments. There’s no point in trying to jump over a 6-foot bar, if hurdling a 1-foot bar will get you same prize. For myself, having followed the company for a short period of time, I feel like I need to send Benioff an expense report for my redundant brain cells.

In a mixture of surprising, and unsurprising events, Slack and Salesforce’s culture have been unable to cohesively meld together, and Butterfield and Bret Taylor (the executive who executed the acquisition) both left Salesforce, apparently for different reasons. So much for the combination being a ‘1 + 1 = 3 situation’. The point being that there is just so much going on here, that it’s basically impossible to figure out what’s going to happen next.

Building on this, it appears that Benioff is extremely flexible in his own approach to managing the company. A group of activist hedge funds have essentially been able to sway him into re-engineering the companies financial profile. While it’s great that they are rationalising operations (remembering that they are still paying Matthew McConaughey $10M a year as a director[?]), what’s going to happen when a new set of institutional imperatives come into vogue in a few years time? Your guess is as good as mine. I’m guessing Benioff doesn’t know either.

This week I also spent a good amount of time revisiting Mauboussin’s Base Rate Book. It’s an absolutely essential piece of investing writing. If you have never come across it, I would highly recommend devouring all 142 pages. Perhaps even in one sitting.

(Link here)

A few highlights that I thought were excellent:

Introduction:

Investing requires a clear sense of what’s priced in today and possible future results. Today’s stock price, for example, combines a company’s past financial performance with expectations of how the company will perform in the future. Market psychology also comes into play. The fundamental analyst has to have a sense of a company’s future performance to invest intelligently.

Understanding Base Rates:

Mauboussin begins the work with an explanation of the Inside View and Outside View. The Inside View is essentially the view informed by expert opinion in a particular field. The Outside View is the view of the statistician. One should apply them based on context:

One way to determine the relative weighting of the outside and inside views is based on where the activity lies on the luck-skill continuum. Imagine a continuum where luck alone determines results on one end and where skill solely defines outcomes on the other end. A blend of luck and skill reflects the results of most activities, and the relative contributions of luck and skill provide insight into the weighting of the outside versus the inside view.

For activities where skill dominates, the inside view should receive the greatest weight. Suppose you first listen to a song played by a concert pianist followed by a tune played by a novice. Playing music is predominantly a matter of skill, so you can base the prediction of the quality of the next piece played by each musician on the inside view. The outside view has little or no bearing.

By contrast, when luck dominates the best prediction of the next outcome should stick closely to the base rate. For example, money management has a lot of luck, especially in the short run. So if a fund has a particularly good year, a reasonable forecast for the subsequent year would be a result closer to the average of all funds.

This is a fascinating proposition and informs my own approach to markets: find situations which are not going to be capriciously influenced by lady luck. Hence, I’m trying to find spots that lend themselves to the inside view.

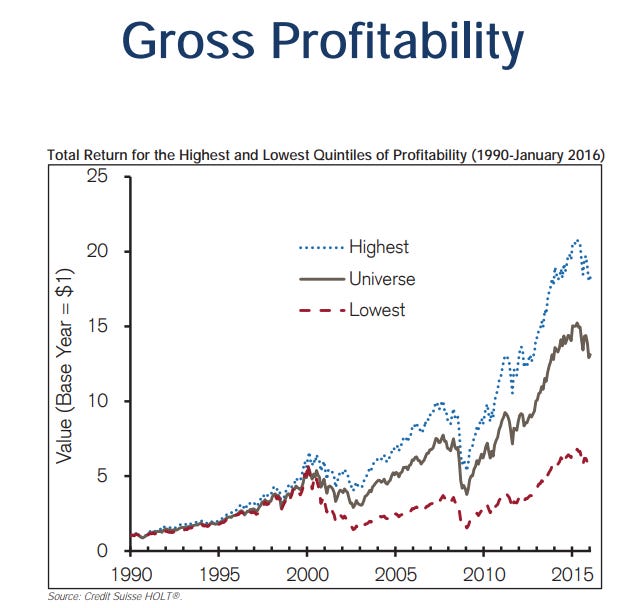

Gross Profitability:

I had never really considered Gross Profitability before, but Mauboussin explains:

Gross profitability is a measure of a company’s ability to make money. Robert Novy-Marx, a professor of finance at the Simon Business School at the University of Rochester, defines gross profitability as revenues minus cost of goods sold, scaled by the book value of total assets. In other words, gross profitability is gross profit divided by assets. Investors can use gross profitability as a proxy for quality and it is not positively correlated with classic measures of value.

Furthermore, it has a fairly strong correlation with market beating returns:

It’s also one of the few metrics which seems to persist over time:

Research shows that gross profitability is highly persistent in the short and long run. This means that you can make a reasonable estimate of future profitability based on the past. Academic research also shows that firms with high gross profitability deliver better total shareholder returns than those with low profitability. This is despite the fact that they start with loftier price-to-book ratios.

The other two parts of the Book were the managing the ‘man overboard moment’ and ‘celebrating the peak’ which discussed a statistical approach to dealing with stocks collapsing and racing to all time highs. To do them justice, I’ll have to deal with them at a later point.

That’s all for this week’s update. Subscribe to keep up with the journey and consider signing up for the paid content if you enjoy longer form pieces.