[Update] FICO: The Melt Up Continues...

An unusual amount of transparency in the Q

Held.

The previous update can be found here.

Fair Isaac Corporation (FICO), reported Q4 earnings late last week. While the results were excellent (yet again), there was an unusual amount of transparency given to investors regarding FICO’s 2025 calendar year mortgage score pricing. The reasons for this are clearly political, and as the price of the FICO’s royalty pricing grows in scores, so too does the risk that political interference may be forthcoming.

The Quarter

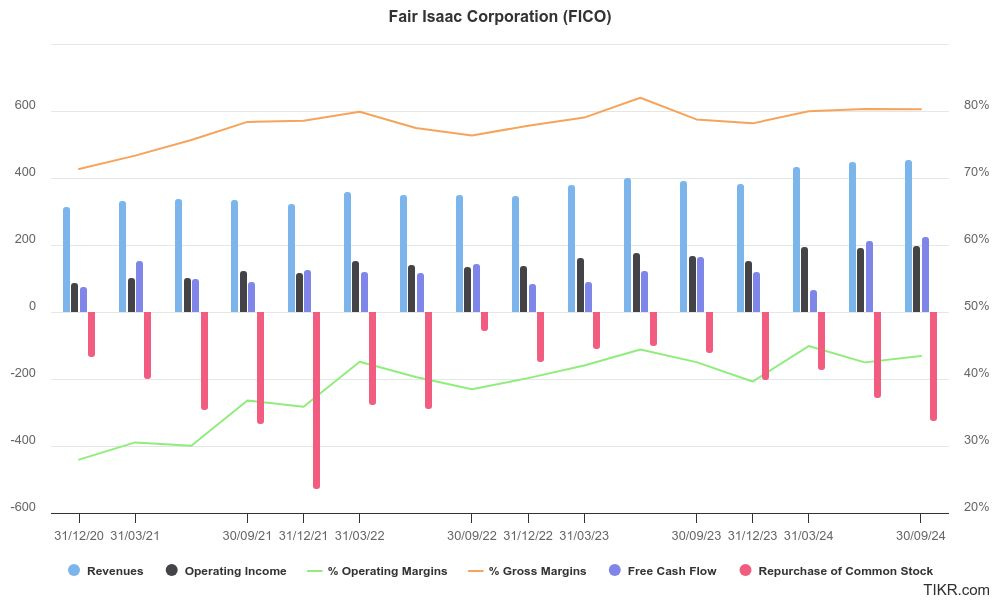

In terms of financial performance, this was another record quarter of revenues, operating income, and free cash flow generation. Gross and operating margins levitated near all time highs (the free cash flow margin hit an all time high of 49.5%), and management has been repurchasing shares at a clip not seen since the depressed share prices of late 2021/early 2022 - a time when their valuation, on a trailing earnings basis, was 1/4th of what it is now and the share price was 1/6th of what is is today.

Overall results looked like the following:

And of course the slide we’re really interested in:

Scores

The dynamic I mentioned last quarter simply seems to have intensified this quarter:

It appears we are now reaching something of an inflection point within an inflection point (I need a moniker for this particular buybackism) - the sheer growth in mortgage Scores revenues, driven by pricing actions (Lansing acknowledged that volumes were once again lacklustre), is bleeding over into Scores revenues generally, with top-line growth breaching the 20% mark YoY! As you should see above and in my previous updates, B2C, auto, card, and personal loans etc have added virtually no incremental business in years (pricing or otherwise). B2B Scores revenue grew 27% YoY.

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.