[Update] Very Difficult Waters for Hemnet

More colour at the turn, and it's not great

In the last update, and indeed in prior updates, I flagged that the moment of truth for Hemnet’s increasingly complicated business development narrative was to occur in April. With nearly three months under our belt of listing data since then, things seem about as murky as ever.

For quick reference, the very singularly poor transaction market of 2025 had been a watershed moment in time for Hemnet’s competition - especially with respect to Booli. With transactions plummeting, and home and apartment prices remaining at heightened levels, a fairly significant shift occurred in vendor behaviour. For the first time, in well ever that I am aware of, large swathes of Swedish vendors flocked to Booli, other smaller portals, and even the likes of Facebook marketplace, looking to gauge the value of their stock, without necessarily looking to sell.

Many critics have been quick to point to Hemnet’s rapidly rising ARPL as the primary causal link to the change in this behaviour. I have not found that to be overly convincing. After all, HEM raised prices significantly in 21’, 22’, and 23’, and there wasn’t any significant change in vendor (or buyer) behaviour. In my opinion, the catalyst to this frankly disastrous turn of events has been in the extreme volatility of the underly transaction market for residential property. HEM simply did not have the product suite to accommodate the bizarre rise of prelistings, and so Booli benefitted from these unusual happenings, and has been able to keep the momentum up, driving very significant web traffic (and listing growth) to their properties in the interim.

To be clear, the ARPL story is undoubtedly a major contributing factor. However, had we remained in a hot transaction market for the last 18 months, I do not think HEM’s main competition would have made the inroads that they have. In a fashion not too dissimilar from FICO, major volume volatility in the underlying market caused very unpredictable externalities, and management (in hindsight anyway) erred by compounding these issues by shoehorning vendors into ever more expensive and unaccommodating advertising packages. For the last year or so many longs have asked themselves the question: “how much worse can it get?” (me included!). Events, at nearly every turn, however, have proved that the answer is: “it can always get worse”.

I. Data, data, data

There are many issues with the data surfaced by Sensor Tower, and by online services like SEMrush and the like. Often they get critical datapoints incorrect (famously for Facebook some years ago). Having said that, most external data sources would confirm that the online traffic advantage enjoyed by Hemnet in the years prior to 2025 has been narrowing with Booli. From a directionality standpoint, Booli grew its online traffic at a very high clip in 2025, and continues to outgrow HEM in 2026. Hemnet has been quick to maintain that they have been growing unique weekly visitors at a predictable clip over the past three years, but it’s not at all clear how much signal is in that.

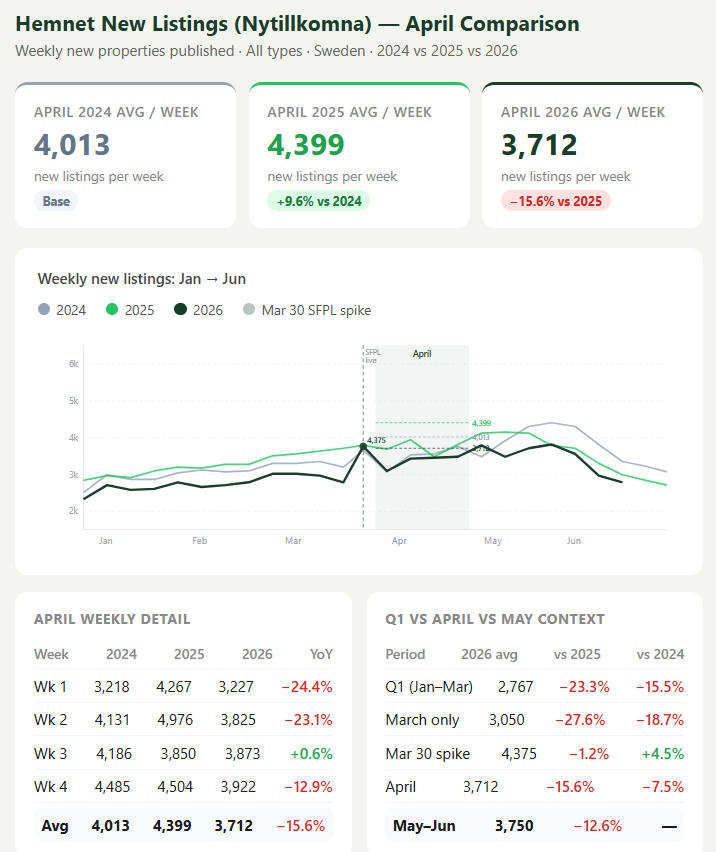

Not picked up in any publicly available datasets are the traffic and engagement numbers with HEM’s app. Other app traffic information is also not easily sourced. In any event, April was promised to be a potential turning point for the residential real estate market more broadly. This was on the back of “credit easing” reforms led by Swedish regulatory authorities, which aimed at adding demand side stimulus for Swedish first home buyers. This coincided with the national roll out of HEM’s sell-first-pay-later model, which initially catalysed the largest ever single week growth in new listings, but which has since appeared to be something of a one-time sugar hit:

As we run into July, incremental new listings are hitting volume levels not seen since before the pandemic. It is notable, however, that the leading local market for HEM’s short-lived listing recovery was Stockholm. You might remember that Stockholm and Gothenburg were the two most enthusiastic adopters of Booli’s prelisting service at the start of 2025.

In my mind, the biggest single (continuing) risk for HEM is that they experience continued sluggishness in the wider transaction market, which maintains this “strange” new status quo. And that very bear case is playing out as I write.

II. The Devil in the (Regulatory) Detail