Weekend Reading & Thoughts

Allan Mecham's Arlington Value Capital, Hetty Green, Excess capital and what I've been doing with it (a special situation)

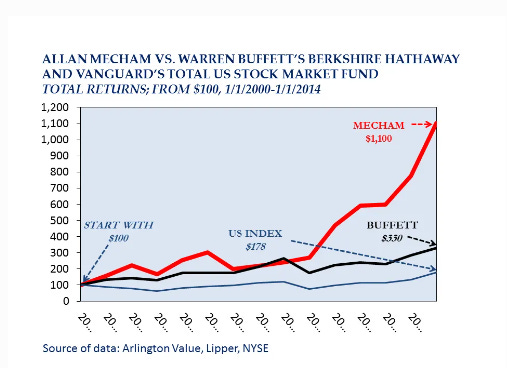

Arlington

I first read the Arlington Value Capital (AVC) letters around the time Allan Mecham began to wind down his fund in 2020. I’m expecting most readers to be aware of Mecham and AVC - for those of you who are less than familiar with the story, it is so intrinsically “value investing” that if it wasn’t true you’d think it was made up.

Mecham began AVC in 1999 at the ripe age of 22 after dropping out of college. While starting an investment partnership in ones early 20s is certainly contrarian, Mecham also operated far away from any kind of financial centre, and far away from anywhere important altogether - Salt Lake City. This is reminiscent of many dyed-in-the-wool value investors, but Mecham took it a step further yet - his “headquarters” was located above a taco shop. It was almost too good to be true.

It was true, however - and the results are just what you’d expect of a person who is so emblematic of the core value investing tropes:

Reading through the publicly available AVC letters, it’s not easy to pin down Mecham’s strategy. His default positioning was to buy high quality businesses trading at attractive prices (no surprise there) - over the years these included Berkshire Hathaway (held), AutoZone, Bank of America, XPO Inc, and Philip Morris International. Mecham’s definition of what a high quality business was very much mirrors my own:

During 2008 we added just two significant positions, both of which enjoy dominant competitive positions and durable advantages. Both companies sell low priced products/services, characterized by stable demand with ample pricing power. I’m particularly drawn to these types of businesses, as they should do well in both inflationary and deflationary environments.

Many of the names he invested in over the years would be uninvestable for many in the wider investing fraternity. Names like Sandridge Energy for example. AVC also had no problem holding large amounts of cash, or holding securities that had unique exposures. Case-in-point, AVC posted positive returns during the GFC years by having a large cash allocation and owning Fairfax Financial Holdings Ltd.

While our conservative culture and philosophy may have held back our performance in years past, it showed merit in 2008. The linchpin of our philosophy is to think critically about risk, especially low-probability risks. Our old fashioned style embraces humble skepticism and is wary of most modern risk management tools and ideas (i.e. broad diversification, financial models, derivatives, etc). Our concern is such tools and ideas can act like mental shortcuts and subtly diminish one’s appetite for critical thinking.

AVC 2008 Annual Letter

With every re-read of the letters, I find that I resonate ever more with some of Mecham’s general precepts. For example:

When we analyze a business, we pay close attention to the qualitative and intangible variables – such factors are often difficult to ‘model’. We are uneasy with fancy numerical models and broad diversification, which have almost ubiquitous acceptance by the high priests of modern finance. In both cases we believe one is susceptible to gaining a false sense of security, which can result in mental slothfulness and neglect. In the case of models, analysts tend to overweight what can be measured in numerical form, even when the key variable(s) cannot easily be expressed in neat, crisp numbers.

AVC 2008 Annual Letter

I had an interesting conversation with an investing friend of mine recently on this very question. From time to time, mostly younger analysts will approach me with detailed models of some of the companies that I follow. They are often horrified when I have comparatively little to contribute to their detailed spreadsheets, and they are positively mortified when I tell them I don’t model in any kind of serious way. Many of you might be getting queasy at this very moment! I understand that in many ways we (that is me personally and many of the professional analysts who I talk to) are playing different games. They are trying to add value in the context of their professional lives - I am simply trying to make money. Modelling is fine (I guess) but it’s not necessarily going to help you make a quid.

Some people know the price of everything but the value of nothing.

We’re handicapping horses, we aren’t performing open heart surgery or sending rockets to Mars. Dealing with dynamic probabilities in real-time is extremely difficult, and the easiest way to come to terms with it in a no-called-strike game is to simply wait for obvious disparities in price and value. If you need to perfectly nail operating results 7 years out to make money, you can safely move onto the next opportunity.

On the issue of the Margin of Safety, Mecham also made an insightful observation:

We think our philosophy is an intelligent way to invest – regardless of whether we’re characterized as ‘growth’ or ‘value’ investors. Such style-box definitions are not germane to stock picking success. Success is based first, on the accuracy of analysis, not style categorization; and second, upon not overpaying for the business in question. The traditional ‘margin of safety’ concept, often emphasized by ‘value investors’, has utility and is something I consistently apply, however it is secondary, and the value is dependent upon solid business analysis.

“It is better to know nothing than to know what ain’t so” – Josh Billings

AVC 2008 Annual Letter

While I personally do not quarrel with the quantitative approach to value investing (the evidence that it is value added is overwhelming), I do not practice it. I do not believe that the future is path dependant, I believe it is contingent. In business the future is contingent on the actions of management teams, on the incentives they operate under, on the decisions of regulators, and a thousand other dynamic variables besides. From time to time the variables to which a business are subject come to together in such a fashion as to offer immense value to continuing shareholders. On occasion we are smart enough to recognise this. Certainly this was the way that Mecham invested - many of his investments went on to have incredible results over a 5 and 10 year time period. Price was the downside protection - business results provided the returns.

Hetty Green

If Mecham’s taco shop office and remote locale tickles your fancy, you’ll be positively delighted with the story of one of Berkshire Hathaway’s original incorporators, Hetty Green. Somewhat pejoratively called the ‘Witch of Wall Street’, Green is another of these historical figures who doesn’t seem real. A proto-value investor who preceded Graham, her achievements are all the more impressive when you consider she lived at a time when women couldn’t vote, couldn’t be a director of a company, and who were regularly at the whim of a trust officer when they did come into wealth.

Henrietta (hence Hetty) Howland Robinson was born on November 21, 1834 in New Bedford. The Robinson side of the family had become wealthy in the whaling business and so Hetty was the heir to a significant fortune. Her personality and proclivities are the stuff of legend.

Green’s most enduring personality trait was her wholesale rejection of societal norms. This was most pronounced by the fact that she wore old, and often tattered clothes her entire life, despite her family’s wealth and station. Even in later life, she would only ever have the hem of her clothes cleaned to avoid wasting money unnecessarily.

At the age of 20 years old, Green’s father sent her to New York to mingle with high society. He hoped desperately that Hetty would find a husband there too, a path in life that she had so far shown zero interest in. The real outcome of this particular trip was that Green returned to New Bedford having only spent $200 of the $1,200 budget her father had provided. He was delighted to find out that she had invested the balance in high quality bonds!

Green’s eventual husband, Edward Green, was independently wealthy, but proved to be a disappointment to his wife: he got caught up in the railroad bubbles of the late 1880s. Investing in the stock of Louiseville & Nashville Railroad (L&N), Mr Green ended up losing a significant fortune (and incurring a significant amount of margin debt) when management proved to be a fraud. Hetty was called on to cover the debts of her husband (to the tune of about $700,000!) after which she changed banks and banished her husband off with a small allowance. A nearly unprecedented marital circumstance for the era.

Green never had her own office. She worked out of the lobby of the various banks where she kept her assets. Paranoid, she suspected that she was being poisoned by her various bankers. Particularly sensitive to living expenses, Green only ever rented small apartments on the periphery of New York City, and eventually =moved to New Jersey to avoid property taxes. Her rejection of creature comforts was the result her Father who claimed to only ever smoke 4c cigars because trading up meant he’d eventually succumb to the hedonic treadmill. His rationale: if you can sustain your standard of living irrespective of the economic cycle, then you can invest successfully through it too.

Green’s investment philosophy revolved around scepticism and contrarianism. She was completely impervious to brokers and promoters, shunning them her entire life. The first principle of her long-time success was complete and accurate information.

Before deciding on an investment, I seek out every kind of information on it.

Her second principle focussed on taking advantage of the crowd, rather than being ruled by it.

I buy when things are low and no-one wants them. I keep them, just as I keep a considerable number of diamonds on hand, until they go up and people are anxious to buy them.

The Gilded Age was a time of excessive and conspicuous consumption. It was also a time when financial markets were characterised by panics. Green lived through several of them, and ultimately learned to profit from them by being reasonably liquid her entire professional life. Green was a major lender to various levels of government, and played an important but quiet roll in JP Morgan’s amelioration of the Panic of 1907.

It is speculated that Hetty ended her long life with a fortune of between $100M-$200M, largely derived from judicious investments in fixed income securities. At the time of her death in 1916 she was almost certainly the most wealthy individual woman in the world.

Excess capital, and what I’ve been doing with it (a special situation)…

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.