Amazon's Quality Inflection Intensifies

Amazon's Quality Inflection Intensifies

Cutting costs, raising prices, investing where appropriate (3PL and AWS)

The ‘steadying’ of Amazon’s ship under CEO Andy Jassy has taken further meaningful steps of late. With each intervening quarter, the modus operandi becomes a little clearer. It’s familiar to me, and it smacks of the historical case studies I have explored in the newsletter already.

")

Firstly, an observation. The pure breadth and scale of Amazon’s services make detailed analysis of minutiae all but an exercise in futility. Collecting anecdata on a handful of merchants or surveying software developers on the efficacy of a certain AWS offering is all well and good, but it can lead to a kind of myopic hyper-fixation. This is exactly where many analysts have veered off in the last couple of years. Famously, Terry Smith’s Fundsmith dumped Amazon after Jassy made some comments about the “opportunity” [read with heavy sarcasm] available in grocery:

We bought Amazon when it was on its way down from the highs of the pandemic, having basically extrapolated the growth of e-commerce demand and built facilities for demand that wasn’t going to be there for the next year or two - and that was all good. We’ve always liked the Amazon Web Services business, and so we didn’t have to worry about all that. Then the relatively new Chief Executive, Mr Jassy, made remarks about wanting to go big in grocery retail, online. Which in our view is disastrously stupid, I’m afraid. So we sold it. We may of course have done a disservice by being very vocal about that… but he hasn’t actually done it. So the thing we worried about hasn’t occurred.1

The quarterly earnings calls are emblematic of this as well. It wasn’t until last quarter that we saw more than a peripheral interest from the analysts in the non-AWS reporting segments. While myopia reigns, for good reasons and bad mind you, what has mattered is what’s been moving the dial on profitability.

The panoply of updates, press releases, and news flashes about the company are enough to inspire an Amazon-only newsletter. However, some of the major updates have been encouraging. Historically, I have not had a problem answering the question ‘what will happen’, but answering the ‘when will that happen’ is a decidedly harder excercise. As an example, I bought my first tranche of AMZN 0.00%↑ shares in the April of 2022, 41% north of the bottom in the stock price. With that being said, sometimes developments can de-fog the front windshield. Amazon’s recent conduct has given me a lot of conviction in their trajectory as a business for the foreseeable future.

Retail

Certainly, some of the recent changes made in Amazon’s online retail business have been significant.

Originally slated for the 1st of April were the new (and controversial) low-inventory fees. This is of course for those merchants who participate in Amazon’s Fulfilled-by-Amazon (FBA) programme. FBA has become less of a service to merchants and more of an absolute necessity to be successful on the 3rd party marketplace. The reason for this is simple. For merchants to be Prime-eligible (and hence have their products available for the lightening fast delivery times promised to Prime customers) they must participate in FBA. This little value-nexus has been a particularly fruitful place for Amazon to take price in the past.

The nature of Amazon’s 3rd party marketplace is that it’s available to almost any merchant who desires to use it, and they pay for access to the marketplace via commissions and fees taken out of the sales dollars they earn. As Amazon handles money upfront, and then remits that money to merchants, they control virtually the entire transaction. Their ability to affect (and get compliance to) price changes is marvellous.

These low inventory fees are aimed at incentivising (maybe penalising) those merchants who have consistently low levels of inventory for in-demand products. In another sense, it’s a way for Amazon to charge the merchant for their own supposed loss of revenue in aggregating demand for a product which couldn’t be sold. Talk about market power - I’d like to get paid for sales that would have occurred ‘but for the merchant imperfectly forecasting demand’ too. It’s also important to mention that this kind of fee is naturally opaque - Amazon made the decision to credit back these fees in April to:

help our selling partners learn in real-time if they need to make adjustments to avoid the fee in the future, while having the peace of mind that during the transition period any fees incurred will be credited back.2

Amazon has had a long history of rolling out continual adjustments to the slew of fees charged to merchants, although they are typically well communicated. The above fee change was first announced in December.

The low inventory fees have been coupled with a change in the outbound service fee. Some context here will be helpful. Historically, a merchant would deliver the entirety of their product to a single Amazon facility. Amazon would then handle distribution to other fulfilment centres and warehouses. While Amazon has sophisticated processes for the distribution of products based on demand (and the 100s factors that feed into that), they would still incur transportation costs on behalf of the merchant. Merchants would then be charged a single outbound service fee.

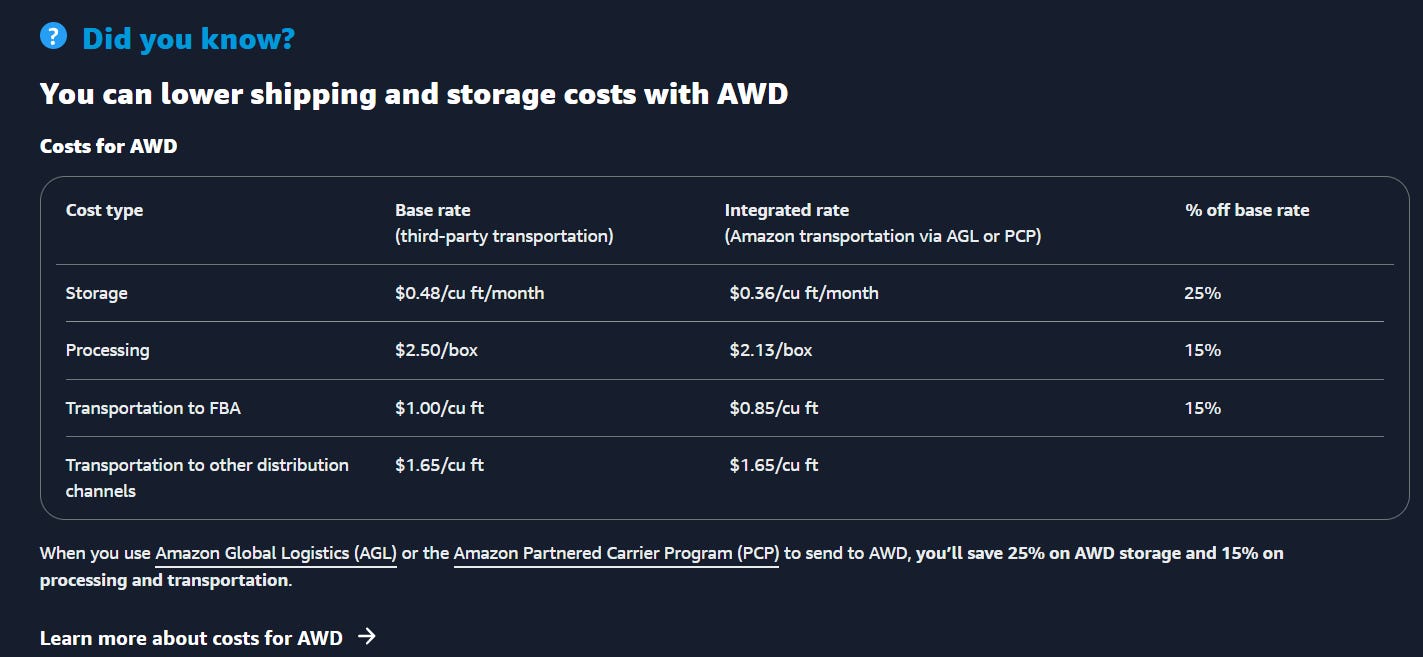

In place of the new inbound fees, merchants can enrol in Amazon Warehousing and Distribution (AWD):

As to whether or not AWD is actually fee saver is yet to be seen - most merchants can’t truly gauge the impacts of these costs until they get some mileage under them. The response from merchants, however, is invariably the same - in a recent Fortune article, interviewed merchant Albert Grazi said:

I’m gonna comply and send [my inventory] into AWD. And that’s it.

In the same vein as Amazon getting to have its cake and eat it too with the low inventory fees, the purpose of this particular fee change is to incentivise merchants to ship their products to multiple Amazon distribution centres across the country OR to sign up for AWD. Where there was once a singular outbound distribution charge, there is now an inbound distribution charge and an outbound distribution charge. One way or another merchants will pay for their products transportation pre-fulfilment.

In large part, these changes have come off the back of the company’s regionalisation efforts. Moving from one national (that is to say North American) distribution regime to one broken down into 8 regions has been paying major dividends on literally every front with respect to retail:

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.