Duff & Phelps

The logic of the asset light business

If you enjoy this piece, you might enjoy reading my original piece on Moody’s as introductory material:

As is customary for the start if year, I’m offering 25% off all annual subscriptions. This offer lasts for the next two weeks. Annual subscriptions really help support the blog and ensure that I’ll be able to continue with it long term.

“Ultimately, business experience, direct and vicarious, produced my present strong preference for businesses that possess large amounts of enduring Goodwill and that utilize a minimum of tangible assets.”

Warren Buffett, 1983 Berkshire Hathaway Annual Letter

As is my usual practice, I start the year off by revisiting some of my favourite educational investing materials. I’m obviously a huge Buffett and Munger stan, but, pragmatically, Joel Greenblatt’s materials have had the single greatest impact on my investing style. As is often the case, Buffett has provided the ideological super-structure under which other practitioners have filled in more granular detail.

Before Moody’s became a standalone company in 2000, another credit ratings business found its way to public ownership in the mid 1990s - Duff & Phelps. Now owned by Fitch Group, this ratings business is a classic example of what’s possible when extraordinary corporate activity meets a great business.

The Spirit of the Age

Although relatively few of us were generally cognizant at the time (or even around for that matter), the heady days of the mid and late 1980’s catalysed an amount of corporate activity that is hard to relate to today. Perhaps only in the throws of the dot com bubble, or the SPAC frenzy of the pandemic-era have we experienced something even remotely similar. As interest rates hit a generational top in 1982, a new breed of financial engineer was liberating capital from an overly capitalised corporate America and directing it towards a merger and acquisition frenzy - the age of the leveraged buyout.

Although Michael Milken was under indictment by the end of the decade, the era he encapsulated persisted for a time.

D&P was founded in 1932, an auspicious year for financial services companies. What started as an investment research service, eventually morphed into credit ratings, and later investment management. By the mid 1980’s at least one external buyout offer had been seriously made. Then in 1989 management (sponsored by private equity) bought out the company. The transaction was highly levered, in part financed by the use of junk bonds. The demands of high-coupon finance and the private equity interest affected an IPO by 1992.

As D&P began to focus on its then core operations - corporate advisory and investment management - its smaller, although much higher quality, credit ratings arm was slated to be spun out. In 1994 shares of Duff & Phelps Credit Rating Co. (referred to as Credit Rating) were separately issued to existing shareholders and they began trading on the New York Stock Exchange.

The Destiny of an Also-Ran Rating Agency

As is now clearly evident, credit ratings agencies are excellent businesses. This is exemplified by Moody’s and Standard & Poors. As the dominant providers for credit ratings globally their brands infer a lower cost of capital on those borrowers looking to tap corporate bond markets. This is a self reinforcing cycle that enforces the leadership position of both of those brands. However, it does leave open a question as to the prospects for an also-ran credit rating outfit.

The market for credit ratings (and here we’ll specifically address the US) is a natural, but also regulated oligopoly. Regulated in this sense doesn’t mean price regulation. The US regulatory authorities acknowledge a handful of companies as Nationally Recognized Credit Rating Agencies (NRCRA). In the mid 1990’s this was a group of some six separate agencies. This has somewhat consolidated in recent years (D&P Credit Rating as a separate brand no longer exists and operates wholly as part of Fitch), but the fact remains that new competition is limited by government fiat.

By Credit Rating’s own admission the scope of their business operations was already extensive in the mid 1990’s:

Credit Rating estimates its comparable 1996 revenues to be equal to approximately 15 percent of the revenues of its largest competitor. Credit Rating's market penetration in the United States, however, is believed to vary significantly depending on market sector. For example, Credit Rating has an inconsequential share of the municipal and mutual fund rating market as historically it has not actively competed in this segment. However, Credit Rating believes its share of the rating business for insurance company claims paying ability, structured financing, and certain segments of the corporate market is much more meaningful. Specifically, in the United States market, Credit Rating has issued claims paying ability ratings on 82 percent of the 100 largest life insurance companies. Credit Rating rates approxima tely 70 percent of the companies comprising the investor-owned electric utility industry and 75 percent of the largest telephone companies. Of banks and finance companies, Credit Rating rates 80 percent and 66 percent, respectively, of the 50 largest companies. Credit Rating also rates 47 percent of Fortune 100 industrial companies.

Duff & Phelps Credit Rating Co., 1996 Form 10K

Starting in the late 1970’s multiple ratings agencies began to be used in the ratings of single issues. This kind of limited global supply but multi-use of incumbents represents a perfect equilibria for a collaborative oligopoly. As more international markets began tapping the vast US debt markets, and the complexity and range of products exploded, especially structured finance and mortgage backed securities, there was more than enough to go around outside of the industry leaders:

Credit Rating believes that significant growth opportunities continue to exist for the following reasons: (1) generally low market penetration; (2) the growing use of multiple agencies for ratings; (3) the increasing number of new financial instruments which require ratings; and (4) the growth of international financial markets. Moreover, as part of its strategy to grow, Credit Rating has established joint ventures with partners in certain North and South American and Asian countries and South Africa (see "-- International") and has offices in London and Hong Kong.

Duff & Phelps Credit Rating Co., 1996 Form 10K

Quality by the Qualitative

In physical terms, credit ratings are a form of human labour arbitrage. The main cost in producing credit ratings is the cost of hiring and retaining an analyst. What makes it attractive from the perspective of the equity holder is the human labour element is completely interchangeable, and clients resonate with the corporate identity. Individual ratings can result in billions of dollars in funding. Value accrues accordingly.

There are relatively few fixed assets needed, and as the value of ratings have grown generally - for instance the advent of structured products grew the value of ratings grew diametrically - so too did the price that was charged for them. Because of the oligopolistic market structure (explained above) those customers who wish to access US debt markets have no choice but to be rated. Hence there’s very little, if any, marketing spend necessary to attract customers. These are all the qualitative elements of a wonderful business.

The Numbers

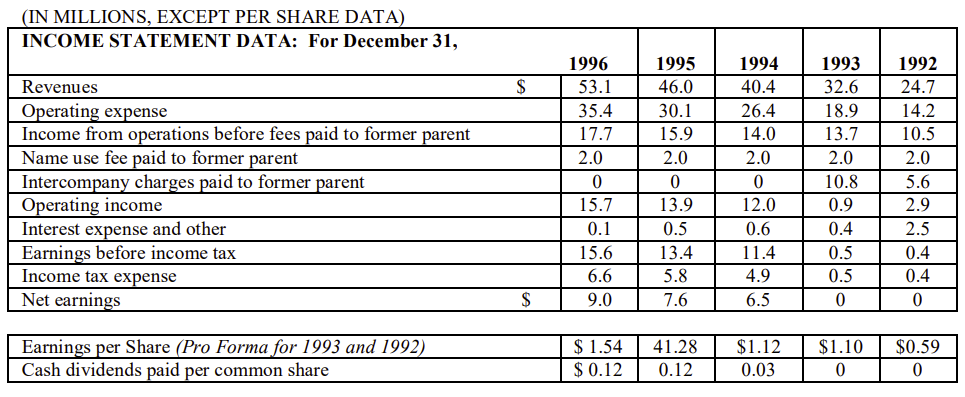

By 1996, the underlying quality of Credit Rating was vividly evident in their reported numbers:

Over the period that spanned the original D&P IPO, and the subsequent spin off, Credit Rating grew its top line revenue at more than 20% a year. Underlying EBIT (before fees paid to the former parent) grew by a modest 14% per year, with margins naturally taking a hit with large step ups in operating expenses (backend operations, legal, and compliance etc) from the spin date. Impressively, this financial performance was achieved by no more than 240 employees - another Buyback Capital favourite.

Likewise, the above was accomplished with only a relatively modest rise in tangible assets:

Even more to the point, the capital allocation side of the equation was unambiguously good. From the moment they were able to, management used every single excess dollar to repurchase shares:

These numbers are even more impressive when contrasted against the valuation from the spin out. Credit Rating was spun out with 5,625,000 shares outstanding at $7 per share. The market capitalisation was $39,375,000. A credit ratings agency growing top line revenue at 20% a year trading for a less than one times sales and a little more than three time operating income!1 I dream.

Repurchases, growth with limited reinvestment, secular drivers, pricing power, and a modest valuation. In 2000 Fitch took out the business for $100 per share - more than a 14x in 6 years.

Goodwill, Inflation, & Physical Assets

Greenblatt uses the D&P example to contextualise Buffett’s own comments on the role of physical assets in certain inflationary environments.

You can live a full and rewarding life without ever thinking about Goodwill and its amortization. But students of investment and management should understand the nuances of the subject. My own thinking has changed drastically from 35 years ago when I was taught to favor tangible assets and to shun businesses whose value depended largely upon economic Goodwill.

This bias caused me to make many important business mistakes of omission, although relatively few of commission. Keynes identified my problem: ―The difficulty lies not in the new ideas but in escaping from the old ones.‖ My escape was long delayed, in part because most of what I had been taught by the same teacher had been (and continues to be) so extraordinarily valuable. Ultimately, business experience, direct and vicarious, produced my present strong preference for businesses that possess large amounts of enduring Goodwill and that utilize a minimum of tangible assets.

Warren Buffett, 1983 Berkshire Hathaway Annual Letter

I feel as though this point is understood today, but probably not as well as it could be. There are obviously important differences between accounting goodwill and economic goodwill. The former represents, in part, the non-capitalised value above which someone has paid for the value of tangible assets in an acquisition. This gets carried on the balance sheet as goodwill, and is amortized over time - i.e. charged against reported earnings as per the relevant accounting principles. Economic goodwill represents the portion of economic value captured (and that could potentially be captured) that deviates from the economic clearing value of the inputs to a product or service. Buffett explains:

In 1972 (and now) relatively few businesses could be expected to consistently earn the 25% after tax on net tangible assets that was earned by See’s – doing it, furthermore, with conservative accounting and no financial leverage. It was not the fair market value of the inventories, receivables or fixed assets that produced the premium rates of return. Rather it was a combination of intangible assets, particularly a pervasive favorable reputation with consumers based upon countless pleasant experiences they have had with both product and personnel.

Such a reputation creates a consumer franchise that allows the value of the product to the purchaser, rather than its production cost, to be the major determinant of selling price. Consumer franchises are a prime source of economic Goodwill. Other sources include governmental franchises not subject to profit regulation, such as television stations, and an enduring position as the low cost producer in an industry.

As inflation is a permanent feature of capitalist democracies - and any other form of economic organisation for that matter - a minimum of fixed assets coupled with significant and, importantly, growing economic goodwill represents the best constellation of features in a business. Where physical, and not intangible, assets are the source of economic output this represents significant risk for the equity holder. Periods of prolonged inflation present the owners of a business with a conundrum: do they invest more capital to maintain returns, or face the prospect of dwindling returns in lieu of reinvestment?

The owner of a franchise isn’t faced with any such challenges. In extreme cases, a large amount of underlying economic goodwill can even be an advantage for such a company in an inflationary environment.

I continue to pound this lesson in.

Larry.

P.S. - As is customary for the start if year, I’m offering 25% off all annual subscriptions forever. This offer lasts for the next two weeks. Annual subscriptions really help support the blog and ensure that I’ll be able to continue with it long term.

I’m happy to be proven wrong here, the numbers don’t sound quite right.

Interesting to compare the main points you make in this article with a business like ODFL:

- Has a strong competitive position in LTL with network effect barriers to entry

- Brand has excellent reputation and delivers a premium service, so business has pricing power

- Evidenced by average post-tax ROIC of 25% over past 8 years, and has compounded FCF/sh by 26%, even while LTL industry has been in recession since mid 2022

- Yet, this is a capital-intensive business, with capex averaging 16% over past 8 years. There are no intangibles and no goodwill (asset base is purely PPE).

Seems like there is a certain special class of asset intensive businesses where the asset base is a source of competitive advantage and growth reinvestment in that asset base continues to grow the moat over time...

Not as high quality a financial model as a FICO or credit bureau but an interesting counter-example to the thesis of looking at asset light businesses!