[Research]: Fannie and Freddie's Hidden Monopoly

The Common Securitization Solution & The Future of Private-label MBS

Not a public company… yet.

In one of my earliest Substack posts I stated something to the effect of: “America is peculiar in that it is the only country in the world that privatises assets that definitely should not be publicly owned.”

Well, here we go again.

After calling into question FICO scores pricing, demanding the resignation of the sitting Federal Reserve Chair, firing the entire senior management layer of both Fannie and Freddie (GSE’s), current FHFA Director Bill Pulte disappeared from Twitter for 13 days. The Book of Genesis tells us that God rested on the seventh day after creation - the Director seems to have had a little more stamina.

I can hardly think of an executive agency that is more in need of a faceless bureaucrat than the FHFA. However, we are where we are.

Perhaps bored with his hiatus (enforced or not), he’s recently reappeared on Twitter with even more colour. After announcing that he’s directed the GSE’s to take crypto currency holdings into account when analysing a borrower’s assets, and claiming that a former GSE employee tried to blow up a federal building that he was visiting, he made the following post:

Edgar Allen Poe might have written “A Dream Within a Dream”, but this might be a special situation within a special situation. A potential demutualisation within two companies owned themselves by the tax payer via warrants? It’s almost too delicious.

I’ll come back to “why?” and “how?”, but I think the first question has to be: “What the hell is CSS?”.

When the taxpayer effectively nationalised the GSE’s during the Great Financial Crisis (GFC) via both Enterprise’s entering Conservatorship, Congress both erected institutions to oversee the GSE’s, and passed a number of laws granting Treasury and the newly formed Federal Housing Finance Agency (FHFA and now U.S FA) extensive oversight powers. This accompanied the agreement that oversaw Treasury’s provision of capital to the GSE’s. In 2012, on the eve of the GSE’s returning to significant profitability, the Obama Administration unilaterally altered that agreement affecting the net worth sweep. Scandalously (and of dubious legality), the net worth sweep deprived both Enterprises from properly recapitalising. To help reduce the government’s liability in the secondary market for mortgages (which they were now acutely exposed to) a number of solutions were floated to open the market up to private participants.

Amongst these executive and legislative attempts to rationalise the GSE’s, in 2012 the FHFA determined that:

that the back office systems by which the Enterprises securitize mortgages were outmoded and in need of being immediately upgraded and maintained.

Status of the Development of the Common Securitization Platform - Federal Housing Finance Agency Office of Inspector General

The FHFA consequently directed the GSE’s to jointly create the Common Securitisation Platform (CSP) to replace a number of outdated back-end processes. The FHFA also established a separate corporate identity, Common Securitisation Solutions, LLC (CSS), to own and administer the CSP. CSS was established with a Board of Managers, conspicuously without a chairperson nor a chief executive. In 2014 two senior executives were appointed by the FHFA to oversee the project.

Curiously, the OIG later commented that:

FHFA envisioned the CSP as a way to maintain liquidity in the mortgage market that would outlive the Enterprises’ current structures.

We’ll come back to that.

There were a number of challenges that the FHFA and the two primary GSE’s faced in getting the project off the ground. The first problem was that no one had the initiative, or authority to properly implement the project. The FHFA was itself a small, embryonic agency at the time, balancing numerous responsibilities. The FHFA had virtually no institutional history, let alone a history of completing large projects. Fannie and Freddie, however, had a notorious history of catastrophic project implementation, as well, of course, as abetting the single largest housing collapse in recorded history. These challenges, however, went further than the purely logistical - the processes that were targeted for automation were varied and specialised.

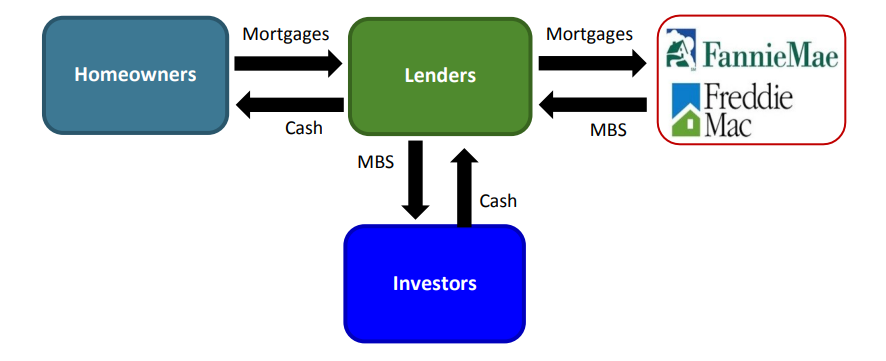

The GSE’s main business is in the securitisation and insuring of residential mortgages. They now also provide this service in the multi-family lending segment. The process for this is fairly straight forward. Lenders originate mortgages fitting a certain criteria (referred to as a “conforming mortgage”), they take these mortgages to Fannie Mae or Freddie Mac and either exchange them for either mortgage-backed-securities (MBS - a bundle of mortgages securitised and insured by the GSE’s), or cash. Where a conforming mortgage is exchanged for cash, the Enterprise will then securitise and insure that mortgage and sell it along to investors. Borrower, lender, Enterprise, investor:

Fannie and Freddie make money by charging a fee for insuring the mortgages they securitise and resell/exchange (referred to as a g-fee), lenders have a pretty incredible product to offer borrowers, and investors (ostensibly anyway) get to purchase high-grade, securitised mortgages without necessarily taking on the risk of any single borrower. That’s the idea.

Prior to the CSP, the business of issuing, and administering these MBS by the GSE’s was conducted by each via their own proprietary internal “tools”. The CSP was planned with the aim of focusing on five distinct business functions: Data Acceptance, Issuance Support, Disclosures, Master Servicing Operations, and Bond Administration.

Data Acceptance is:

the process by which the Enterprises validate 6 loan level data associated with mortgages they pool and plan to securitize. For example, the Enterprises confirm that zip codes of the mortgaged properties are expressed in the correct format, i.e., in nine numbers. The Enterprises also confirm that the underlying mortgages conform to certain of the Enterprises’ MBS rules.7 For example, with a 30-year fixed-rate security, the Enterprise will verify that all of the loans in the underlying pool contain the appropriate characteristics.

Issuance support is the process of offering MBS to investors:

To initiate this process, the Enterprises transmit to the Federal Reserve Bank of New York basic facts about the security, the prospectus, and their initial disclosures. The Enterprises publish initial disclosure information simultaneous to the security issuance.

Disclosure is the process by which the Enterprises publish statements for their MBS investors that describe the securities issued and the characteristics of the underlying mortgage pools. The Enterprises publish disclosures using monthly data provided by servicers.

Master Servicing Operations:

The Enterprises serve as master servicers for the MBS they issue. Master servicing functions include the collection and reconciliation of loan data reported by the servicers. For example, the Enterprises compare their own calculations of expected monthly principal and interest payments with the amounts reported to them by servicers each month.

Bond administration:

Is the process by which the Enterprises ensure that payments associated with their MBS are calculated and distributed appropriately. Bond administration includes calculating the monthly principal and interest payments for MBS. As part of this function, the Enterprises generate MBS performance metrics that are included in their monthly MBS disclosures.1

The CSP would eventually be launched in June 2019, a full 7 years after it was commissioned, and 9 years after Fannie Mae launched their own internal efforts. Fannie had even looked at outsourcing these functions to a third-party but (auspiciously) no provider could be found, and no out-of-the-box software solution existed either.

It’s also important to note that the Obama Administration’s efforts to spur the development of the CSP was to build a utility-like product that would assist private-label MBS providers return to the market, and one day (“hopefully”) supersede the GSE’s. President Obama originally saw the Enterprise’s days numbered, right up until the point that they became a profit centre for the government. The opening up of the CSP to the private market never eventuated simply because the private market for MBS really never recovered to what it had been. The GFC effectively ended that market, and the nature of Conservatorship gave the GSE’s a bigger competitive advantage than they ever could have dreamed of beforehand. When it’s in his interest Uncle Sam is as ruthless a capitalist as I have ever known.

The services that the CSP now provides to the Enterprises is somewhat more limited in scope than what was first envisaged. This mostly covers administering and issuing MBS. One of the neat things about the CSP is that it has essentially standardised how single family MBS are issued. At its inception it wasn’t expected that the CSP would serve multi-family MBS products, and it was hoped that it would be flexible enough to accommodate emergent mortgage-backed products de novo. It’s rather unclear if this has actually come to pass, but ultimately it hasn’t mattered. It now issues the so called UMBS (universal mortgage backed security) which is a common security issued by both Fannie and Freddie.

Keep reading with a 7-day free trial

Subscribe to Buyback Capital to keep reading this post and get 7 days of free access to the full post archives.