Updates #4

EFX (held), FICO (held)

Equifax (held)

I posed a number of questions about Equifax’s forward trajectory in my last update. Last week’s quarterly results and earnings call seem to have remediated a number of those concerns, proving once again that on general direction I am pretty good, but on specific development timelines I am horrendous. The story progresses, and these transitionary periods between operational and capital allocation regimes remains a recurring source of opportunity for the long term investor.

The company led the release with perhaps the most impactful part of the update:

With strong free cash flow and balance sheet, the Board of Directors authorized a $3 billion share repurchase program expected to be completed over 4 years and a 28% increase in the second quarter dividend to $0.50 per share.

Equifax Q1 2025 Earnings Release

This has been a long awaited development for investors, and its the beginning of the company’s reversion to a much cleaner set of financials, which will more closely resemble its profile before the data breach in 2017:

Unfortunately, this is not capital allocation a la William Lansing:

The 28% increase in our dividend reflects our confidence in the new Equifax business model and moves our payout ratio to about 25% of 2025 adjusted net income. Going forward, we plan to increase dividends annually in line with earnings generally in the first quarter of each year and about in line with the expected growth in adjusted EPS with a range of 5% to 15%.

Our new $3 billion share repurchase program announced today reflects repurchases we expect to make under normal market conditions to be completed over the next 4 years, while continuing to maintain a strong balance sheet, continue to invest in Equifax through CapEx and bolt-on acquisitions and consistently grow our dividend in the future.

We intend to be in the market consistently during EFX trading windows and will flex up share repurchases during periods of stock dislocations and flex repurchase levels up or down based on bolt-on M&A activity. And as free cash flow accelerates in the future from operating leverage and lower CapEx spending and as the mortgage market recovers, we expect to increase the level of cash we return to shareholders versus our share repurchase program.

Mark Begor, Equifax CEO, Q1 2025 Earnings Call

Naturally, if you’re a believer in EFX as a long term proposition you’d be more comfortable with share repurchases. After all they allow for much more flexibility in terms of timing and ability to cease them if/when the time came for it. Dividends cannot be scaled up and down easily, they are a long term commitment. In any event, it’s much for muchness.

EFX expects long term capital expenditures of between 6-7% of revenue, and to continue to do opportunistic, bolt-on M&A:

Third, to continue to execute our bolt-on M&A strategy at 1 to 2 points of revenue growth focused on bolt-on acquisitions aligned with our strategic priorities around unique data assets, strengthening workforce solutions, identity and fraud, and new international platforms like Boa Vista.

Continuing to acquire data assets for EWS/TWN is an undoubtedly good use of shareholder capital, but appropriating resources for EFX’s international business continues to be a head scratcher for me and many others. Given the choice between repurchasing shares in an entity dominated by EWS or deploying that capital into a rag tag collection of businesses with an operating margin in the single digits, I know which one I would pick.

Broadly speaking, the narrative of EFX transitioning from a mature credit bureau hampered by ever increasing capital commitments and suspect, larger scale M&A to a much more dynamic proprietary data provider with a predictable regime of capital returns is in tact. However, and as I have said before, this transition is not going to be a straight line up and to the right.

In light of this, there’s certainly no denying that EFX is a little less quality (overall anyway), and a little less growth than I would typically be interested in. This quarter’s revenue growth topped out at 4% YoY, and rather more disappointing at the operating and net income levels and free cash flow.

YoY gross and operating margins stood virtually unchanged. While there are positive developments happening outside of mortgage it shouldn’t be a surprise to anyone that a large degree of the latent operating leverage in the business is sequestered there. As developments in Washington continue to overtake the domestic US economy, we’re left asking the rather awkward question of: ‘when is the normalisation coming?’

My answer is a fairly sullen: ‘at some point’. If, yes. When, I’m not so sure.

One of the thoughts percolating through my mind has been how the current environment will affect record aggregation at EWS. I have explained before how EFX/TWN has a kind of 'fattest wallet wins’ dynamic with respect to its competitors. Data lead > record hits > more revenue feedback to record supplier > scale > larger % of revenue feedback can be handed to record supplier while maintaining economics.

Developments on this front have been very positive as of late. Management have been talking up the recent partnership with Workday, which advantageously integrates TWN with Workday Payroll. Begor, also noted the aggregation of another 3 million active records in the quarter which brings EWS’s total active records to nearly 191 million, and almost 751 million in total. Continued very strong momentum here underlies much of EFX’s overall long term opportunity.

EFX also rolled out a combined credit file and verification/TWN product. An aggregation to the second power product, if you will. As far as I’m concerned, these kind of developments are a pretty clear example of EFX expanding their moat and offering bespoke solutions that their competitors at the TWN level (funded or owned by TransUnion and Experian) will find it very difficult to compete with. Proximity to the credit file, coupled with their significant proprietary lead is a very interesting combination.

Interestingly, USIS outgrew EWS on a percentage basis, with the latter experiencing significant headwinds in employer services:

EWS:

Total revenue was $618.6 million in the first quarter of 2025, up 3% compared to the first quarter of 2024. Operating margin for Workforce Solutions was 42.7% in the first quarter of 2025 compared to 42.3% in the first quarter of 2024. Adjusted EBITDA margin for Workforce Solutions was 50.1% in the first quarter of 2025 compared to 51.1% in the first quarter of 2024.

USIS:

Total revenue was $499.9 million in the first quarter of 2025, up 7% compared to the first quarter of 2024. Operating margin for USIS was 21.1% in the first quarter of 2025 compared to 19.9% in the first quarter of 2024. Adjusted EBITDA margin for USIS was 34.1% in the first quarter of 2025 compared to 32.7% in the first quarter of 2024.

This somewhat anomalous situation is a continuation of what EWS has observed in the back end of last year. As interest rates for residential mortgages have come down somewhat - 70bps in the first quarter as per EFX - there has been a significant uptick in hard pull activity which takes some time to filter its way down to verification. These revenues have also had the additional tailwind of passing through FICO’s special price increases which continue at pace for now. Importantly, management suspended any future guidance updates - that is they’ll be sticking to the guidance they gave in February - citing volatility in various end markets as a result of the current administration’s economic policies.

Unfortunately shares bounced hard on the earnings announcement, so we’ll have to see next quarter just how many shares they were able to repurchase, and in any event prevalent prices are not terrible.

FICO (held)

As Michael Corleone famously lamented: ‘just when I thought I was out, they drag me back in’.

That is, of course, a reference to my coverage of the name, and not my holding in it.

The big news, of course, was that the special pricing regime officially entered a new phase today:

I am reading the above as a 10-15% price hike in Automotive Scores, in the first quarter of this year.

Since at least the back end of 2021 it is fair to say that the non-Mortgage related Scores reporting segments have remained unchanged with respect to pricing. The reason for this is a little hard to say; my initial thoughts were that they probably couldn’t take significant pricing in these areas. In fact I remember making this very case to a subscriber in a café in New York, almost to the day, last year.

Another school of thought would be that FICO were waiting for a more benign interest rate environment before taking price outside of Mortgage. In retrospect it was probably best for management to focus on the most inelastic source of demand during a time of relative turbulence across lending markets. Well, here we are 3+ years later and we are witnessing special pricing at a mere fraction of what we have seen in mortgage.

What do I make of this?

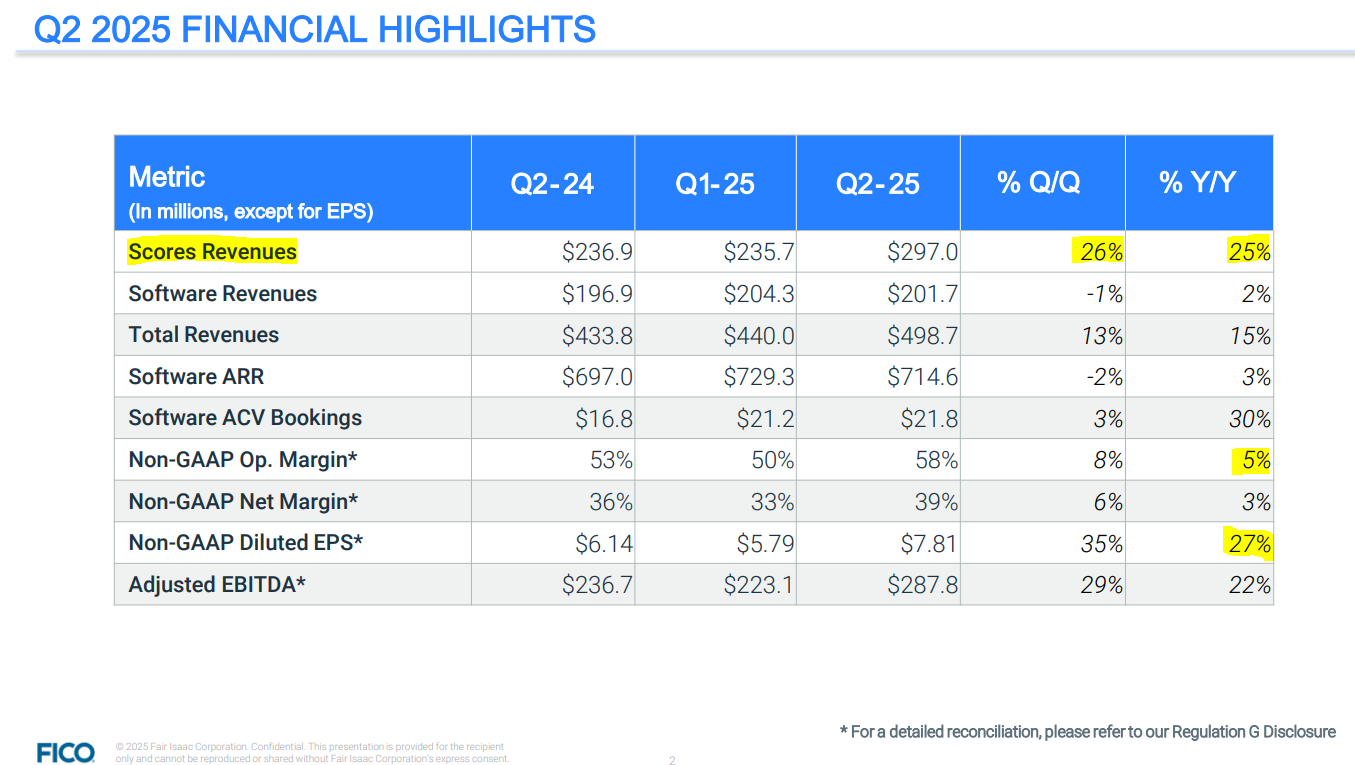

I think we’re very early on in this particular game. There’s probably a decent chance that management is simply testing the waters out in Automotive specifically. The pricing actions in Mortgage over the last few years has incurred political and industry backlash, although none that has significantly altered FICO’s pricing trajectory. Enough though, in any case, that Lansing felt it necessary to pen two blog entries defending the company’s conduct. For shareholders, at least, this is a very positive development which has added another dimension to Scores ability to generate pretty incredible revenue growth and earnings contribution. Behold:

It needs no repeating that each additional dollar of Scores revenue is ridiculously high margin and is very accretive to margins and earnings. As Mortgage related scores revenue laps the large increases that we have seen over the past few years, it is still encouraging to see healthy growth in that segment too. In any event, the rate of B2B Scores revenue growth is still bleeding into group revenue acceleration (15%) despite the pretty woeful quarter for software, and especially platform.

Also intriguing is the positive numbers in B2C revenue. This is, of course, a leading indicator for credit activity widely - an individual is likely only checking her own credit score in anticipation of a serious credit application. This sits in nicely with EFX’s own reading in its USIS segment - with rates coming down across Mortgage refinancing activity will pick up at pace.

On a somewhat mundane note, share repurchases pulled back slightly from the 4th quarter of 2024. We will have to see how management reacted to the volatility in the early April sell off next quarter.

The work of normalising FICO’s earnings just got a little more complicated. Without wanting to sound like a completely rusted on bag-holder, my common retort to those lamenting/lambasting FICO’s sky-high present valuation is to simply ask that person what they expect normalised mortgage volumes and pricing (that is on a bundled basis, as is) to be. To be sure I am often confronted with blank stares at this point, but now I’ll be able to pose a secondary set of considerations: what do you expect normalised Automotive volumes and pricing to be? If we can’t always be right, we can be annoying.

It’s anyone’s guess as to where this might be. We are coming off a relatively low base, but at this point I think we can say that Automotive revenues as a portion of Scores B2B revenues is in the range of 15-25%. You can apply your own expected pricing rate and duration to see where we might get to. In any event it’s a positive development.

I will continue my own ambivalence to the Software side of things. It appeared that some nice bookings growth was weighed down by some short term factors which led to Software’s first YoY revenue decline in quite some time. With Scores doing so much of the heavy lifting now, it becomes a little less of an urgent consideration by the quarter.

Larry.

As a slight aside, Finchat has kindly been sponsoring the blog. This helps enormously with my research, and charting - and you’ll know I’m fond of both. For a long time I was an ardent user of TIKR, however, the comparison with Finchat isn’t close. If you’d like to try it out for yourself using the link here. For this week only there is a 25% discount on subscriptions - so you know what to do.