Issue No. 27: Pricing Power - Investing Philosophy Part 1.

The key to long term investing success

“The single-most important decision in evaluating a business is pricing power.”

Warren Buffett

When you shout something out, you also pound it in. That is exactly what I am doing in this week’s Issue.

While the general market environment has been a little dull when it comes to serving up investment opportunities - this piece will be part of a multi-part series covering the tenets of a quality purist’s approach to markets.

A General Observation

For the most part, investors are not focused on the variables that really matter over the long term. Most people are caught up in a meta-game of trying to anticipate the factors that other investors in turn are anticipating. What’s the guide? Did growth come in below or above expectations? Was the CEO caught on a on a mega-yacht with his Mistress?

If you really owned a business, and weren’t just renting the shares for a quarter or two, would you really care about others expectations about it’s performance? I’ve known plenty of CEOs and Directors in my time, and most of them really only care about the strategy, and then the bottom line.

However, when one owns shares in publicly traded securities, speculation and conjecture are par for the course. The broader public and large institutions measure what is easily reported. Many managements and IR teams love to flaunt growth rates, TAM opportunities, market penetration, and adjusted EBITDA numbers that don’t easily correlate with the value being derived for shareholders. During the earlier growth phase of a company these might be the only numbers that really tell you anything at all.

Growth, in all of it’s forms, can be either good, bad, or even neutral. For example the rapid growth and spread of cancer is a terrible thing. On the other hand, a teenager experiencing a growth spurt is expected.

Pricing flexibility, however, is almost never made readily available by management teams, and IR departments go out of their way to obscure it. A Thielism is instructive here:

All monopolies pretend not to have a monopoly, all commodity businesses pretend to have a monopoly.

The first reason for this is obvious. Price hikes are wildly unpopular and provoke hostility in a businesses customer base. If a firm finds itself at sufficiently large scale, that hostility can transmute into adverse regulatory action. Almost every legal jurisdiction in the world has a regulatory regime tasked with curbing anti-competitive behaviour. Regulated pricing, of various kinds, permeates even the freest markets.

Many markets which are serviced by a duopoly or an oligopoly will also wish to obscure their pricing behaviour. It’s not hard to cry ‘collusion’ under such transparency.

Finally, no company wants to advertise how wonderful it’s own business is to energetic and well funded would-be competitors. To copy another phrase: competition and capitalism are antonyms, not synonyms.

A simple truth remains: the only free lunch in business is the ability to raise prices in excess of inflation without incurring a relative loss of demand.

Businesses which have a constant need to reinvest capital into their operations, and who are price-takers, are especially at risk during inflationary times.

How to Identify Pricing Power

Price elasticity has been studied for over 140 years. In fact, Alfred Marshall coined the phrase in 1890. It was adjoined by the following illustration:

There are several sub-factors that can influence how much pricing elasticity a product has with it’s consumers:

Addictiveness: Also explained in psychology as chemical dependency. Addictive products make the postponing of it’s consumption painful. This creates a predictable consumption pattern. Cigarettes and branded caffeinated beverages are the obvious examples. Nicotine and caffeine have powerful withdrawal symptoms and create pleasure through consumption.

Brand Loyalty: Chemical dependency, along with other psychological biases, can also result in brand loyalty. Consumers associate (another psychological tendency) a brand with an emotion. For example, they feel good when they consume a particular brand of cigarettes and feel terrible when they don’t.

Passed Along Costs: Many B2B services have a large degree of pricing indifference as the cost of a product is passed onto an end consumer. This is seen through products like the FICO score, where the Credit Bureaus pass on the cost of the Score to the borrower. The advertising agency of a bygone era were compensated on a cost-plus basis of ad-buys they completed on a customers behalf. Perversely, they were incentivised to spend more.

Value Based Pricing: Sometimes the gap between the tangible value provided by a product and it’s actual monetary cost are so great as to make even relatively large price increases seem trivial to customers. This is also seen in products which result in cost savings for customers. So long as pricing remains low enough to make the cost saving economic, prices can be raised.

Necessary or Mandated Products: Some products and services are mandated by law or by the marketplace. This swings the balance in favour of suppliers during negotiations.

The above factors will not translate into profitable operations unless the following microeconomic factors are expressed by an individual firm (i.e the franchise business):

The firm produces a good or service that is desired or needed by it’s customers,

That has no readily available substitute,

With unregulated pricing power.

Some confluence of the above factors, combined with the hallmarks of a franchise business (which comes first, the chicken or the egg?) - should result in very clear pricing power.

The Hallmarks of Pricing Power

Richard Lawrence gives us the following excerpt on how to identify pricing power in the financial statements:

Where do we go on the financial statements to identify pricing power? There are two components that are really important. Firstly. the Gross Margin, or even one above it - the Cash Gross Profit Margin. Depreciation can vary by company, we don’t know if everyone is going to depreciate everything equally. You go to your Cash Gross Profit Margin, and that’s going to reflect where your pricing decisions are going on. Then you are looking for consistency, low standard deviation of your Cash Gross Profit Margin, and so your best guys in the world have high Gross Profit Margins but also very little variability.1

Richard H. Lawrence Jr.

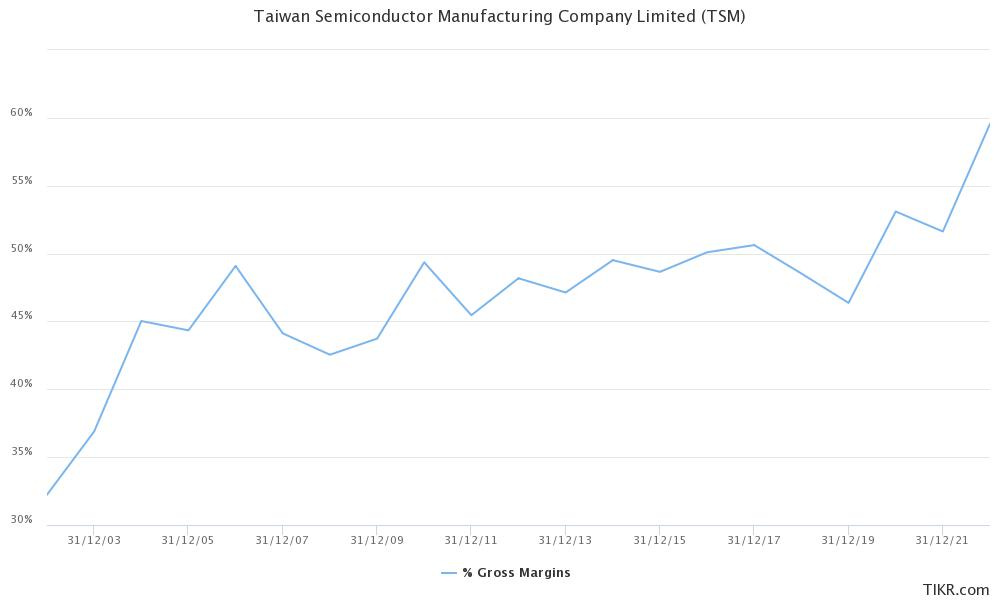

The example that Lawrence gives is Taiwan Semiconductor Company. While the talk was given in 2015, this particular example was especially prescient:

Anyone with a properly functioning brain stem could tell you that the semiconductor industry is, broadly speaking, cyclical. TSMC’s ability to defend their Gross Margins over a period of time that has seen several upheavals speaks to a simple fact: they aren’t compelled to compete on the basis of price.

We can take it a step further. They have actually grown their Gross Margins through several cycles - including the current challenging environment. It’s amusing to think that TSMC’s Gross Margin eclipses Alphabet’s - you know, the asset light compoundoor?

While stability in Gross Margin’s is good, expanding Gross Margin’s are even better. The very best businesses grow all their margins over time. In the end, the ability to raise prices is the only path to long term excellent economics.

A Wrinkle in the Formula

Some products, counter-intuitively, derive demand from increased prices. The association bias is at play here. The human mind sometimes associates quality with price, and so for a certain subset of products low prices signal poor quality. This is especially true for luxury apparel, and vehicles. After all, if someone offered you a Bugatti for $1,000 your first question would be: what’s wrong with it?

Munger talks about a slightly different case where this is true:

This happened in the case of my friend Bill Ballhaus. When he was head of Beckman Instruments, it produced some complicated product where if it failed it caused enormous damage to the purchaser. It wasn't a pump at the bottom of an oil well, but that's a good mental example. And he realized that the reason this thing was selling so poorly, even though it was better than anybody else's product, was because it was priced lower. It made people think it was a low-quality gizmo. So he raised the price by 20% or so and the volume went way up.

This is also observed in products like infant formula:

If you’re a parent you know about infant formula and what a racket it is. It’s an oligopoly. It’s so expensive here in the U.S. that sometimes supermarkets will lock up the formula behind a glass case. So, it’s an industry that has really interesting characteristics. A few companies dominate shelf space because they participate in the WIC Program. The WIC Progam is a program for babies that are born into poverty and there’s State contracts, and if you win the contract you get all the shelf space in that State, and you end up making your profits from the other half of the parents [who aren’t participating in the program]. The dynamic that plays out in infant formula is that the highest the cost, the higher the perceived quality the parents think they are getting. In fact the ingredients in infant formula are regulated and they are essentially the same. If there’s two formulas on the shelf and one is $5 and the other is $10, the parents will buy the $10 one because they think there’s something better about it.2

Dev Kantesaria, Valley Forge Capital

The desire for high grade (or perceived high grade) infant formula is so strong that Chinese students and visitors to Australia actually hand purchase it from supermarkets and fly it back to mainland China (see the history of A2 milk).

I have experienced this phenomenon myself. Over a year ago the company I worked for tried to roll out an affiliate program with no upfront implementation costs. It failed miserably and got zero initial traction until we started charging up front fees. The human mind is a strange thing.

Frequency of the Purchase

No matter how vital a product is you’ll only very rarely find customers willing to sign contracts with preset pricing escalators. It’s somewhat easier for a firm to push pricing down the line with small ticket, repeat purchases. Quite often buyers won’t even realise there has been a rise in price. Buffett has been raising the price of confectionery at See’s Candy every year on December 26 without any meaningful interruption to volumes since 1972.

Renegotiating service agreements at regular intervals can be difficult. Aspen Technologies (a firm spun out of an MIT laboratory that provides crucial industrial management software) offers clients 6 year licence agreements with yearly pricing and seat escalators that take inflation into account. Those are particularly favourable, and are a testament to the need for the software and the lack of any meaningful competition. While lurking on a Reddit forum I saw that Canada’s Dye and Durham offers expiring clients 3 year renewal deals, with set price increases per transaction on renewal.

The as-a-Service-ification of everything (from software to logistics) is a way to ease these dynamics. A typical SaaS-model now moves pricing to a monthly amount - be that per seat, by transaction, or whatever other quantum is appropriate. This allows for more efficient pricing communication, but it also comes at the cost of allowing clients to leave at shorter notice - often 30 days. This was recently displayed by Toast, Inc. (a POS and restaurant management SaaS platform) who had to completely backtrack on an announced pricing increase. Toast CEO Comparato said it all:

While we had the best of intentions—to keep costs low for our customers—that is not how the change was perceived by some of you. We made the wrong decision and following a careful review, including the additional feedback we received, the fee will be removed from our Toast digital ordering channels.3

Three things make price hikes acceptable in my experience- and I should know I’ve negotiated hundreds of these:

The difference between the value provided and the increase proposed is significant,

The customer has a favourable attitude toward the company and/or the company’s representative. It’s especially important that customers feel like they have a feedback channel, even if it doesn’t result in them actually getting anything,

There’s an available mechanism for passing on some (or all) of the cost to end customers.

That’s all for this week.

Larry.

https://www.saastr.com/toast-we-crossed-the-line-on-price-increases/

I like AZPN quite a lot, I think it looks pretty interesting long term. A lot of potential there

Great, looking forward to the other parts.

What is generally better, smaller frequent or less frequent larger price increases to keep customers?